Legalising the theft of Russian assets

There are, I’m afraid to say, still too many truly believers in the Russia total defeat delusion. Ukraine can still win! With what troops and, critically, what money?

With Glenn Diesen, Ian Proud. Nov 10, 2025

Following my recent article on the topic of the so-called EU reparations loan (a cheap ruse to fund the Ukrainian state for another 2-3 catastrophic years of war), I discussed the issue in more detailed with Glenn Diesen,

The more I consider this issue, the more clear it becomes that attempting to exproprirate Russian assets is a desperate measure to prevent EU Member States from giving Ukraine the money themselves, money which they do not have.

The Commission idea, should the Russian asset option continue to be blocked by Belgium, to borrow the money on international markets and then lend it to Ukraine, which can’t borrow money itself, appears similarly desperate. Who will make repayments on that loan? Becauses Ukraine won’t.

Suddenly, the EU idea of common debt becomes more worrying still. Who wants to give Kaja Kallas a blank cheque to fund proxy wars in other countries, with repayments being share among Member States?

Amid all of this, with Pokrovsk falling, Kupiansk and Siversk almost lost, the Russian army pushing into Zaporizhia, does anyone in Brussels take a step back and ask whether, in fact, it would be better to support the US in leveraging Zelensky to settle?

There are, I’m afraid to say, still too many truly believers in the Russia total defeat delusion. Ukraine can still win! With what troops and, critically, what money?

EDF Braces for More Delays at UK Hinkley Point Nuclear Project.

The Hinkley Point nuclear project in the UK, ridden by repeated delays and cost overruns, is bracing for yet more setbacks. The latest schedule for

completion around the end of the decade is likely to be pushed back by at

least another year as operator Electricite de France SA continues to

grapple with the installation of electrical systems, a person familiar with

the matter said, asking not to be named discussing private information. The

delay may stretch for 12 months or more if corrective action plans continue

to prove challenging, another person said.

Bloomberg 7th Nov 2025, https://www.bloomberg.com/news/articles/2025-11-07/edf-braces-for-more-delays-at-uk-hinkley-point-nuclear-project

The $17bn nuclear start-up without any revenue

A nuclear technology company backed by Sam Altman is riding a wave of investor enthusiasm

Publicly-listed Oklo sits at the intersection of two hot areas for Wall Street: artificial intelligence and energy companies. This year alone, Oklo’s share price has jumped more than 400 per cent. But the business hasn’t generated any revenue. It hasn’t built a nuclear reactor, and it hasn’t secured any binding contracts with customers. The FT’s US energy editor Jamie Smyth explains the enthusiasm for Oklo, its links to the Trump administration and whether it can live up to the hype. company backed by Sam Altman is riding a wave of investor enthusiasm.

Clips from New York Stock Exchange, The White House, a16z – – – – – – – – – – – – – – – – – – – – – – – – – – For further reading: Inside Oklo: the $20bn nuclear start-up without any revenue US and investors gambling on unproven nuclear technology, warn experts Donald Trump’s assault on US nuclear watchdog raises safety concerns

Subscribers only –https://www.ft.com/content/d87cb0ac-b599-46b9-8a4d-9a8b55541ab2

TRANSCRIPT – Michela Tindera speaks to Jamie Smyth

Nov 5 2025 Audio transcript of podcast.

“……………………………. Jamie Smyth

Oklo’s valuation soared to more than $25bn in just 18 months, and this really caught my eye. I’ve been tracking quite a lot of these smaller nuclear companies over the last 18 months, but nothing had reacted like this.

They want to power the artificial intelligence revolution using nuclear energy, but a new type of nuclear energy, which hasn’t been in use to date in the commercial nuclear world.

Michela Tindera But here’s the thing. This high-flying start-up Oklo, it doesn’t have revenues, licenses to operate, nor does it have any contracts with customers. So what’s going on with this company? That is what Jamie and our colleagues have been digging int

Jamie Smyth Oklo has become a symbol of the AI boom and the ongoing nuclear renaissance because of the astonishing rise in the value of its shares and its close relationship with the Trump administration. How the company fares could have a big influence in whether nuclear energy powers this AI revolution.

Michela Tindera

I am Michela Tindera from The Financial Times. Today on Behind The Money, is Oklo’s promise justified, or is it just riding the wave of AI hype?

Jamie Smythe…………………………………………………………..

So Oklo started in 2013 by a couple called Jacob and Caroline DeWitte……………. back in 2013, they met Sam Altman of OpenAI fame …………………….he decides to invest in Oklo………………….He later agrees to chair the company and steer its stock market listing. Now that happens in May 2024 through a Spac or a special purpose acquisition company deal.

…………………Oklo’s share price initially. In fact, it fell on the first day of the listing. But after Donald Trump’s election, and particularly with his inauguration, he really ratcheted up the focus on energy dominance and also gave this strong support for nuclear power.

…………………….And then in May 2025, you get Oklo’s chief executive Jacob DeWitte visiting the White House and speaking in the Oval Office………….

You have Trump sitting in the Oval Office, launching several executive orders on nuclear energy pledging to quadruple capacity by 2050, and he’s invited Jacob and a couple of other CEOs of nuclear companies. You’ve got the chief executive of Constellation Energy standing there beside him, the chief executive of General Matter, an enrichment company, standing there.

……………The room is really packed full of celebrities and there’s Jacob DeWitte in amongst them all.

Jacob DeWitte audio clip………………… The physics are on our side and these things help unleash this innovation to actually realise that. So it’s never been more exciting.

Donald Trump audio clip

Very exciting indeed. Go ahead, please.

Jamie Smyth This platform to speak from the Oval Office next to Trump, I think was a huge endorsement of the company for investors. You really start to see the stock price jump from there, and then it really goes through the roof. It’s made the DeWittes paper billionaires. They own just under 18 per cent of the company, though they’ve made a large chunk of real money too by selling some of their stock. In the past six months, they’ve made about $250mn in share sales according to some Bloomberg data analysed by the FT.

……………………………….Well, I think Oklo really sits at the intersection of these two stock market booms in artificial intelligence and energy companies. The AI revolutions being driven by Nvidia, Microsoft, Amazon and other big tech giants, and this realisation that data centres, which are driving the AI technology, they’re gonna require huge amounts of electricity. So that’s why you’re seeing shares in energy companies, utilities like Constellation Energy, gas turbine makers such as GE Vernova and Siemens and other nuclear start-ups, all their shares are soaring.

………………………………. the Trump factor. The administration is spending big on nuclear.

Michela Tindera

Like Jamie mentioned earlier, the Trump administration has pledged to quadruple US nuclear capacity by 2050

Jamie Smyth It has very ambitious plans to build out 10 large-scale reactors and support this new technology that Oklo is developing. And specifically, Oklo has benefited from this. They have been offered a place on a fast-tracking programme for their nuclear reactor. They’ve also been offered a place on a fuel programme as well. And they are being given a very specialised, scarce form of fuel, which they require to run their type of reactor. So I think investors are responding to this and they’re getting very excited.

……………………………Bank of America have actually said that this support from the Trump administration is one element that gives the company an edge over its rivals. Democrats, however, have alleged that it really creates an appearance of impropriety, and they have asked a series of questions of the administration about its relationship with Oklo.

………………Oklo wants to build a new type of nuclear reactor, something called a small modular reactor or an SMR…………And what’s interesting about Oklo’s SMR is that it wants to use liquid sodium as a coolant rather than the standard of water.

……………………………Oklo would say their reactor could be safer than a water-cooled reactor in terms of a Chernobyl-style accident. It’s just not gonna happen. But there are downsides to sodium-cooled reactors. You know, the big question with these sodium-cooled reactors are, we’ve had four or five of them actually already built in the United States over the last 40 years on a test basis, but none of them have actually managed to become commercially viable, so they didn’t take off. ……………………………………….

Michela Tindera So Oklo’s plan here sounds pretty ambitious. First, they wanna build a new kind of nuclear reactor that hasn’t been sold commercially in the US before. And second, they also have this untested business model. They wanna sell the nuclear power themselves instead of offloading that to a utility company.

………………..Jamie Smyth

Oklo have a very ambitious goal of commercially beginning to sell power through their SMRs by 2027……………..

They haven’t yet built their nuclear reactor. They haven’t got a licence for their nuclear reactor. They haven’t got any revenue and they haven’t got a legally binding contract with a customer.

Michela Tindera Not any customers at all?

Jamie Smyth They don’t have legally binding par purchase agreements with customers. What they’ve got is they’ve got MOUs or memorandums of understandings. So companies have come to them and said, we’d like to talk about and draw out an outline of an agreement, but there’s no legally binding agreement yet in place. So until it can do that, I think there’ll always be a question mark over the sustainability of the company.

Michela Tindera A lot of what Oklo is pursuing is untested, the technology, but also the business model of both building the reactors and selling the power they generate. And as its market valuation source, analysts are increasingly pointing out that the company’s valuation is stretched.

The business has attracted the attention of short sellers. That’s people who bet on a stock’s price going down. Oklo’s short sellers have borrowed roughly 13 per cent of the stock. They believe that the DeWittes have underestimated the amount of time and money that’s required to commercialise their technology. One area they’ve particularly struggled with is licensing.

Jamie Smyth One of the issues to do with Oklo is, it’s one of the few companies that has had a licence application rejected by the Nuclear Regulatory Commission in the United States. That is quite a big thing.

……………………..Jamie Smyth………….And then in 2022, the NRC didn’t award the licence. So that really raises the question mark about whether Oklo was able to secure one of these licences. Oklo has strongly criticised the NRC decision to not award them a licence. They even alleged the NRC staff engaged in inappropriate behaviour for a regulator.

………………Michela Tindera In the years since, Oklo has successfully lobbied the government to streamline the NRC licensing process. Jamie Smyth So the Trump administration has set up a separate pathway for SMR developers to build test reactors on federal land under the oversight of the Department of Energy, which is run by energy secretary Wright. And beyond that, the Trump administration has piled extraordinary pressure on the NRC to approve reactors within short timeframes, much shorter than previously.

Michela Tindera But as Oklo moves forward, it’s a space that everyone will be watching closely.

Jamie Smyth I suppose one of the risks with Oklo is, if they try to move too fast, they try to race ahead with their technology and they hit a wall, then it could impact the rest of the industry. And this nuclear renaissance that we’re beginning to see could be hurt by that. Safety is of key importance in the nuclear industry. If something goes wrong, you have seen it in the past, then the whole industry suffers.

Michela Tindera So to recap, this is a company with no customers and no contracts, and . . .

Jamie Smyth At the minute the company has generated zero revenue, yet it is currently one of the highest-valued pre-revenue companies listed in the US. And that makes people nervous.

……………………………..Jamie Smyth So the thing about Oklo is, because it’s based in Silicon Valley, it takes a very Big Tech approach to how it’s gonna operate, which is very different than other nuclear companies have worked in the past. You know, move fast and break things is the motto in Silicon Valley.

……………………………………………………………………………Jamie Smyth I think what investors probably want to see is they need to see delivery now. They need to see progress on a licence with the Nuclear Regulatory Commission. Oklo says they’re working towards that, but they also need to see some contracts which are going to bring in some revenue, and most importantly of all, they need to see that these reactors are going to work and that they’re going to work on a commercial basis. ………………….. https://www.ft.com/content/3e84e4d4-bf72-44f7-8fdd-0bdf36c806f6

Bpifrance helps UK nuclear reactor to financial close.

6 November 2025 By Jacob Atkins

French export credit agency Bpifrance is covering a £5bn loan from 13

commercial banks to help finance the construction of the Sizewell C nuclear

power station in England. The facility, structured as a green loan, sits

alongside a £36.5bn term loan from the UK’s National Wealth Fund, which

was announced earlier this year, as well as a £500mn working capital

facility. Bpifrance has secured refinancing from French public development

bank Sfil, according to a November 4 statement. BNP Paribas acted as joint

debt advisor to Sizewell C, with HSBC as French authorities and green loan

co-ordinator, and Santander as documentation co-ordinator on the Bpifrance

facility. The other lenders on the Bpifrance loan are ABN Amro, BBVA,

Crédit Agricole, CaixaBank, Citibank, Crédit Industriel et Commercial

(CIC), Lloyds Bank, Natwest, Natixis and Société Générale.

Global Trade Review 6th Nov 2025, https://www.gtreview.com/news/europe/bpifrance-helps-uk-nuclear-reactor-to-financial-close/

Canadian government happily splashing tax-payers’ money on wasteful things nuclear

Gordon Edwards, 6 Nov 2025

A comment on https://www.msn.com/en-ph/technology/general/the-smr-boom-will-soon-go-bust/ar-AA1PJi1U

This is your ultraconservative radical, Gordon, sounding a note of caution.

The fact that our utilities are publicly owned means that ordinary economic rules need not apply.

The military brings in little or no revenue but the government still funds it.

Gentilly-2 in Quebec was a loser always, and I told reporters to ask Hydro Quebec to give just one good economic reason why the G-2 reactor should not be shut down. No economic reason was forthcoming but the government of Quebec said “we want to maintain a minimal level of expertise in the nuclear field.”

So do not expect SMRs in Canada to be cancelled just because they are uneconomic.

Who cares? It’s not THEIR money they are spending, it’s OURS.

Trump’s Westinghouse Nuclear Fiasco: Wasting Money on a Corrupt Game of Hot Potato.

By now, it is evident that no one is buying Westinghouse’s reactors, so it must be up to the U.S. government to do it. But why?

That still means someone will have to pay the cost of $80 billion-112 billion, plus interest, for loans and/or investor returns, plus the costs of operating, fueling, decommissioning, and nuclear waste storage. Taxpayers will likely pay that cost, too.

On Tuesday, the White House announced an $80 billion deal with Westinghouse to finance construction of eight large new reactors in the U.S. There is not enough in the way of actual details about the deal, resulting in even more unanswered questions. But the promise of a large, direct investment in a pack of new reactors has predictably revved up talk of yet another “Nuclear Renaissance” and made it look like the DJT 2.0 administration is making good on big nuclear power goals from a group of executive orders issued in May.

$80 billion sure sounds like a lot! And the news that the announced $80 billion is going to come from Japanese taxpayers and not U.S. taxpayers sounds like a sweet deal!

If we were talking about just about any other energy source, it would be a lot. $80 billion could build:

- 58,000 megawatts of solar power, or

- 38,000 MW of wind power, or

- 48,000 MW of wind and solar combined, or

- 14,000 MW of geothermal power plants.

Any of those options would produce about the same amount of electricity each year as 14-16 large-sized nuclear reactors – twice as many as the Westinghouse deal promises to build.

But $80 billion is only enough to build, at most, four Westinghouse AP1000 reactors. That’s because the cost of building nuclear reactors is four to 10 times more than wind, solar, or geothermal power. Even wind and solar paired with battery storage are still several times cheaper than new nuclear reactors.

But where would the other $80+ billion for eight reactors come from? U.S. taxpayers? Ratepayers? In this case, probably taxpayers. The reactors would probably receive low-interest loans from the Department of Energy’s (DOE) loan guarantee program, and, following construction, they would be eligible to claim the Clean Energy Investment Tax Credit, which provides a 30-50% subsidy for the cost of a new energy project. That would mean $80 billion or more in loans up front, and, later, $48-80 billion in rebates from U.S. taxpayers.

That still means someone will have to pay the cost of $80 billion-112 billion, plus interest, for loans and/or investor returns, plus the costs of operating, fueling, decommissioning, and nuclear waste storage. Taxpayers will likely pay that cost, too. One of the projects that would probably be included in the deal is the proposed four-reactor Donald J. Trump Nuclear Power Plant (DJT NPP), which former Energy Secretary Rick Perry’s new company Fermi, Inc. has proposed. Fermi’s stock price surged on Tuesday after the Westinghouse deal was announced. The DJT NPP is to be built at the DOE’s Pantex nuclear weapons plant in Texas, to power AI data centers that Fermi also plans to build there. The reactors and data centers are likely to be categorized as “critical defense facilities”, per Executive Order 14299. Presumably, federal taxpayers would pay for the data centers and their power bills through DOE’s budget.

Another feature of the deal is a U.S. government profit-sharing and partial ownership in Westinghouse. The company’s Canadian owners – Brookfield Renewable Partners (BRP, an equity investment firm) and uranium company Cameco – would give the U.S. government a 20% share of Westinghouse profits, after the company earns its first $17.5 billion. Then, if Westinghouse’s corporate value reaches $30 billion, Brookfield and Cameco would have to take Westinghouse public on the stock market – and give the U.S. government at least 8.3% of the company’s stock.

This would benefit Brookfield and Cameco, but not U.S. taxpayers. Another Brookfield affiliate bought Westinghouse from Toshiba when it went bankrupt in 2017 due to soaring costs of building four AP1000 reactors for utilities in South Carolina and Georgia. The South Carolina reactors (V.C. Summer 2&3) were canceled, and the Georgia reactors (Vogtle 3&4) were completed in 2024, seven years late and $23 billion over budget. Brookfield Business Partners (BBP) was unable to sell Westinghouse after pulling it out of bankruptcy, but after countries started sanctioning Russia over its war on Ukraine, it looked like Westinghouse could replace Russia as the largest supplier of reactor fuel and services, so BBP sold the company to Brookfield Renewable Partners and Cameco.

Westinghouse’s value hasn’t exactly seen explosive growth, so it has been seeking deals to sell AP1000 reactors in Poland, Ukraine, Slovenia, the Czech Republic, and other countries, in partnership with the U.S. government, which has become increasingly convinced that it must retake global leadership in reactor construction from Russia and China. The Biden administration tried to convince states and utilities that all of the problems with Westinghouse’s AP1000 reactor had been resolved. But still, no state or utility has taken the plunge.

By now, it is evident that no one is buying Westinghouse’s reactors, so it must be up to the U.S. government to do it. But why? Japan’s offer to pitch in $80 billion will soften the blow to U.S. taxpayers. It may even be enough to build the four reactors Rick Perry wants to name after the president. But we would still end up paying the rest of the cost of too-expensive power and never-ending nuclear waste storage, from reactors that mostly will not be providing electricity to our homes and businesses, but to data centers to power AI. Westinghouse is being passed around like a hot potato and we’ll likely be on the hook when the music stops.

The SMR boom will soon go bust

by Ben Kritz, 3 Nov 25, https://www.msn.com/en-ph/technology/general/the-smr-boom-will-soon-go-bust/ar-AA1PJi1U

ONE sign that the excessively hyped concept of small modular reactors (SMRs) is now living on borrowed time is the lack of enthusiasm in the outlook from energy market analysts, whether they are individuals such as Leonard Hyman, William Tilles and Vaclav Smil, or big firms such as JP Morgan and Jones Lang LaSalle. None of them are optimistic that the sector will be productive before the middle of next decade, and the more critical ones are already predicting that it will never be, and that the “SMR bubble” will burst before the end of this one. My frequent readers will already know that I stand firmly with the latter view; basic market logic, in fact, makes any other view impossible.

In a recent commentary for Oil Price.com, one of the rather large number of online energy market news and analysis outlets, Hyman and Tilles predicted that the SMR bubble will burst in 2029. They based this on the reasonable observation that power supply forecasts are typically done on a three- to five-year timeframe. The fleet of SMRs that are currently expected to be in service between 2030 and 2035 simply will not be there, so energy planners will, at a minimum, omit them from the next planning window, and might decide to forget about them entirely. Deals will dry up, investors will dump their stocks or stop putting venture capital into SMR developers, and those developers will find themselves bankrupt.

That is an entirely plausible and perhaps even likely scenario, but the SMR bubble may burst much sooner than that, perhaps even as soon as next year, because of the existence of the other tech bubble, artificial intelligence, or AI, an acronym that in my mind sounds like “as if.” The topic of the AI bubble is an enormous can of worms, too complex to discuss right now, but the basic problem with it that is relevant to the SMR sector is that AI developers need a great deal of energy immediately. It has reached a point where AI-related data centers are described in terms of their energy requirements — in gigawatt increments — rather than their processing capacity. The availability of power determines whether or not a data center can be built; if the power is not already available, it must be within the relatively short time it will take to complete the data center’s construction.

Even if SMRs were readily available, their costs would discourage customers; AI developers are not too concerned with energy costs now, but they will be as their needs to start actually generating a profit become more acute. On a per-unit basis, SMRs are and are likely to always be more expensive than conventional, gigawatt-scale nuclear plants, and for that matter, most other power supply options. Hyman and Tilles estimate that on a per-unit cost basis (e.g., cost per megawatt-hour or gigawatt-hour), SMRs will be about 30 percent higher than the most efficient available gigawatt-scale large nuclear plants. Being smaller, SMRs would — hypothetically, as they do not actually exist yet — certainly cost less up front than large nuclear or conventionally fueled power plants, but their electricity would cost much more in the long run. That might not be an issue in some applications, but it certainly would if SMRs were intended to supply electricity to a national or regional grid.

Some analyses point out that some early adopters of SMRs, that is, customers who have put down money or otherwise promised to order one or more SMR units if and when they become available, may not be particularly price-sensitive; for example, military customers, governments taking responsibility for supplying electricity to remote areas, or some industrial customers. However, they would still be tripped up by the fragmented nature of the SMR sector, which was caused by the “tech bro” mindset of ignoring almost 70 years of experience in nuclear development and trying to reinvent the wheel.

JP Morgan’s 2025 energy report noted that there are only three SMRs in existence, with one additional one under construction; there is one in China, two in Russia, and the one not yet completed is in Argentina. All of them had construction timelines of three to four years, but took 12 years to complete; or in Argentina’s case, 12 years and counting. Argentina’s project has had cost overruns of 700 percent so far, while China and Russia’s projects were 300 percent and 400 percent over budget, respectively.

These are all essentially one-off, first-of-a-kind units, so some of these problems are to be expected, such as regulatory delays, design and manufacturing inefficiencies, and challenges from building supply chains from scratch. These problems would be resolved over time, except that there are literally hundreds of different SMR designs all competing for the same finite, niche-application market.

If the SMR developers listened to the engineers and policymakers who built up nuclear energy sectors that took advantage of economies of scale by standardizing a few designs and distributing the workload, they might get somewhere. That is not happening; potential customers, whether they have power cost concerns or not, are reluctant to jump in because it is not at all certain which SMRs will survive the competition. They might be willing to experiment to see if one design or another actually works — that is why the Chinese and Russian SMRs exist — but the fragmented SMR sector prevents them from trying more than one and making comparisons, at least not in a timely or financially rational manner.

I think the bubble begins to burst this coming year. The timeframe for construction to startup in most SMR pitches is four years. That’s entirely too optimistic, of course, but even if it is taken at face value, once we get a few months into 2026 without any tangible development happening, everyone will catch on that there won’t be any SMRs by 2030, and interest will turn elsewhere. It already is, among the data center sector, as was explained above.

UK’s nuclear waste problem lacks a coherent plan.

The [GDF] will comprise vaults and tunnels of a size that may be

approximate to Bermuda, but without the devilish tax evaders, coupled with

a 1 km square surface site that will periodically swallow up trainloads of

toxic radioactive waste. It would be unsurprising if Nuclear Waste

Services, the agency charged with finding and building the site, placed a

job advert for its own Hades to manage this dystopic underworld and if the

postholder engaged Cerberus to guard the entrance.

The plan comes with an enormous bill for taxpayers which will scare the ‘bejeebers’ out of taxpayers. Previously the Government’s new National Infrastructure and Service Transformation Authority (NISTA) had identified in its August 2025 report that the GDF facility may have a whole life cost estimated to range from £20 billion to £53 billion.

Now PAC members have had a further frightener placed on them because these headline figures were based on 2017/18 prices and they have found that, when adjusting to the present, the undersea radioactive monster might cost over £15 billion more. It would be far cheaper to hire Godzilla.

The Public Accounts Committee Chair Geoffrey Clifton-Brown has called on the Government to produce a ‘coherent plan’ to manage the UK’s stockpile of radioactive waste

NFLA 31st Oct 2025, https://www.nuclearpolicy.info/news/trick-not-treat-nuclear-dump-is-full-of-nasty-surprises-not-sweet-treats/

Who is paying for Britain’s nuclear revival?

Ultimately, the UK taxpayer is paying for both power stations……………..If Sizewell’s total costs rise above around £47 billion, private investors are not obliged to inject additional equity, leaving the taxpayer exposed to cost overruns.

15th October 2025 by Sol Woodroffe, https://www.if.org.uk/2025/10/15/who-is-paying-for-britains-nuclear-revival/

In this article, IF volunteer Sol Woodroffe, considers the intergenerational fairness of the government’s financing models for Hinkley Point C and Sizewell C.

Building a nuclear power station: an intergenerational decision

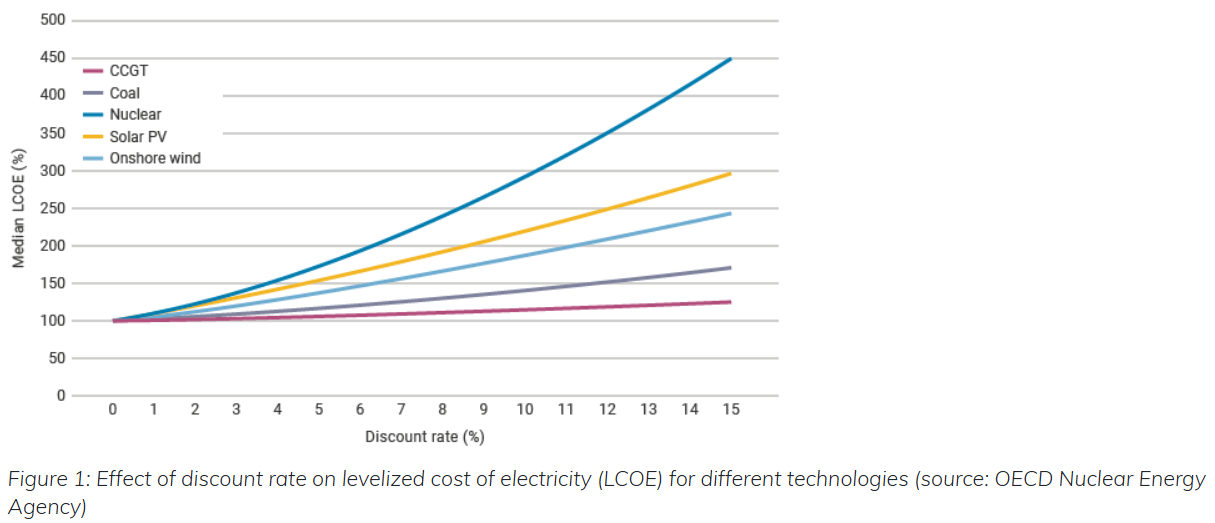

Building a nuclear reactor is very expensive. In fact, the financing costs are the most expensive part. According to the World Nuclear Association, capital costs for new nuclear power stations account for at least 60% of their Levelised Cost of Electricity (LCOE). The LCOE is the total cost to build and operate a power plant over its lifetime divided by the total electricity output dispatched from the plant over that period. This means that when we talk about the price of nuclear, we are really talking about the price of borrowing to cover the upfront costs.

Specifically, when determining whether a government should invest in nuclear power, the cost depends on how much the government values cheap electricity for future generations. The decision to build a nuclear power station is a truly intergenerational one. This graph from the World Nuclear Association highlights how different discount rates affect the value for money of nuclear energy compared with other energy sources:

This shows that the relative capital intensity of building a nuclear power station means that the more we discount future generations, the less worth it nuclear energy seems from today’s standpoint.

The discount rate the government chooses to use on public infrastructure projects is, to some extent, determined by interest rates. But it is also an ethical choice about how much the government cares about future generations. The lower the value placed on future generations, the higher the discount rate used, and so the more expensive nuclear energy seems.

On the face of it, the UK government’s decision to build two enormous nuclear reactors should be a source of optimism for young people. Nuclear energy is one of the safest and cleanest forms of energy. In many parts of the world, it is also one of the cheapest. Decarbonisation, energy security and industrial strategy are all part of the motivation for building these reactors. Many of the UK’s current reactors were built in the 70s and 80s and will retire by the early 2030s. Without new capacity, the UK will lose a major source of low carbon power. Arguably, it’s a sign of the UK government daring to invest for future generations. And yet, a closer look at the financing of the two reactors tells a different story…

What are Hinkley Point C and Sizewell C

Hinkley Point C is the first new UK nuclear station in a generation. It uses the European Pressurised Reactor (EPR) design and, when complete, will be one of the largest nuclear power stations in Europe. According to EDF Energy, each of its two reactors will produce enough electricity to supply roughly 7% of the UK’s electricity demand. Construction was authorised by Theresa May’s government in September 2016. The original target was to have it running by 2025, but EDF now forecasts first power no earlier than 2029–2031.

Sizewell C is a close imitation of Hinkley planned for the Suffolk coast. The UK government approved the development in July 2022 and committed public equity financing in November 2022. Because the Hinkley supply chain and licensing work already existed, ministers argued that a second EPR project would reduce design and regulatory costs. Sizewell C will have enough capacity to power around six million homes when operating.

What went wrong and why?

Both projects are running well behind their initial projected timelines, and both have run worryingly over budget. These two things are interrelated. Long construction periods push up financing costs. Again, the cost of finance here is all-important. Over a long construction period, during which there are no revenue streams from the project, the interest on funds borrowed can compound into very significant amounts (World Nuclear Association, 2023).

HPC’s original cost estimate was about £18 billion but now is projected to a whopping £31–£35 billion. Moreover, our research on the “nuclear premium” estimated the additional cost of power from Hinkley Point C for its 35-year initial contract period, compared to onshore wind and solar power, would be £31.2 billion and £39.9 billion respectively. Sizewell C’s projected cost has ballooned from an initial estimate of around £20 billion to £38 billion (in 2025 pricing), nearly doubling the original figure.

The cause of these cost overruns is clear. EDF has complained that the UK lacks the building infrastructure and productive capacity for such a massive project. This kind of capacity is built up over time and requires beginning with smaller projects and then gradually scaling up. To some extent, the government has acknowledged this mistake and so began to invest in the small modular reactor programme in the UK, but from the perspective of the taxpayer, it all seems too little too late.

Who is paying for these power station?

Ultimately, the UK taxpayer is paying for both power stations. But from an intergenerational fairness perspective, the key questions are which taxpayers and when. The government has an option to borrow and shield the current taxpaying generation from footing the bill, but rising UK borrowing costs and increasingly jittery bond markets mean this would come at a serious cost.

Hinkley Point: paid for by Gen Z and Gen Alpha

The financing model for each power station is very different. For Hinkley point, the government has agreed on a Contract for Difference. This means that private companies must cover the upfront costs, with the knowledge that they receive a guaranteed price for their energy when the costs are finished.

EDF, the French national energy company, and CGN, the Chinese national energy company, shouldered much of the initial capital cost. In return, the government guarantees a price of £92.50/MWh (in 2012 £) for 35 years of output.

There were serious advantages to this model from a public financing perspective. The main advantage was that the investors took on the construction-cost risk: the UK taxpayer has arguably not been punished because Hinkley Point’s financial costs have so enormously overrun.

Nonetheless, this model ultimately kicks the financial burden down the road. Ultimately, today’s Gen-Z and Gen Alpha will be made to pay for this deal.

This is because the guaranteed price will likely be a rip-off. The average price of energy today in terms of 2012 pounds is £50–55/MWh. The falling price of clean energy alternatives means that we should expect the real price of energy to fall over the next few decades. Therefore, it seems highly likely that the fixed price will be a seriously uncompetitive rate for future UK consumers.

Sizewell C: a fairer distribution of costs

The financing of Sizewell distributes the financing costs more fairly between generations. To pay for the reactor, the government switched to a Regulated Asset Base (RAB) model. This means that consumers begin contributing to the project’s financing through small charges on their energy bills while the plant is still under construction, rather than waiting until it generates electricity. The model provides investors with a regulated return during construction, reducing their exposure to financing risk.

The RAB model allows investors to share construction and operational risks with consumers, which in theory lowers the cost of capital. Since capital costs make up the majority of nuclear project expenses, this could make Sizewell C substantially cheaper overall, if delivered as planned.

The key drawback is that taxpayers and consumers shoulder significant risk. If total costs rise above around £47 billion, private investors are not obliged to inject additional equity, leaving the taxpayer exposed to cost overruns.

From an intergenerational fairness perspective, the financing model is somewhat fairer as it smooths the cost of construction between generations. Nonetheless, the future taxpayers are the ones most exposed to the risk of cost overruns.

The cost of decommissioning

Historically, the cost of decommissioning nuclear power stations has been gravely underestimated in the UK. Decommissioning costs will be faced by generations well into the future, and so whether the state considers them massively depends on the chosen discount rate. Ultimately, the more the government values future consumers, the more seriously they must take these massive costs.

Sizewell and Hinkley both have operating lives of 60 years. However, with Sizewell, future taxpayers are exposed to the risk of ballooning decommissioning costs, whereas with Hinkley the operator must fully cover these costs.

Think of the children

When these large public infrastructure projects are discussed, the focus is often on whether government has negotiated value for money for UK taxpayers. But if the government wants to claim nuclear is a forward-looking investment, it must prove future generations won’t be the ones footing the bill.

“It is unacceptable that the EDF tariff reform is being adopted quietly, to the detriment of the users”

With electricity bills reaching record highs and 7 million people facing

energy poverty, it’s time to acknowledge the failure of a model. Twenty

years of brutal energy sector liberalization have failed to bring about

either lower prices or the investment promised by private operators in

exchange for regulated access to historical nuclear electricity (ARENH).

Created in 2011 to allow alternative suppliers to purchase EDF’s nuclear

production at a fixed and highly advantageous price, this mechanism was

supposed to generate sustainably competitive offers. On the contrary, it

has led to instability, private rent-seeking, industrial fragmentation, and

debt for EDF.

Le Monde 29th Oct 2025,

https://www.lemonde.fr/idees/article/2025/10/29/il-est-inacceptable-que-la-reforme-des-tarifs-d-edf-soit-adoptee-discretement-au-detriment-des-usagers_6650111_3232.html

Starmer,Macron, Merz…3 unwise leaders degrading their economies while destroying Ukraine.

President Trump has largely ceased supplying weapons directly to Ukraine. But he’s cool about goosing US weapons builders’ profits by selling them to Europe’s Big 3 so they can take over squandering their treasure on an impossible, quixotic effort to defeat Russia.

Walt Zlotow, West Suburban Peace Coalition, Glen Ellyn IL ,1 Nov 25

The UK’s Keir Starmer, France’s Emmanuel Macron and Germany’s Friedrich Merz are wildly unpopular. Starmer has the best approval rating at 13% followed by Macron at 11%. Merz is nearly invisible at 5%.

There are several reasons but likely tops is their insistence on continuing the lost US/NATO proxy war against Russia destroying Ukraine for nearly 4 years.

President Trump has largely ceased supplying weapons directly to Ukraine. But he’s cool about goosing US weapons builders’ profits by selling them to Europe’s Big 3 so they can take over squandering their treasure on an impossible, quixotic effort to defeat Russia. Trump, a realist on the war Biden made inevitable, wants out, not only on funding the war, but on endlessly funding Europe’s paranoia about a reconstituted Soviet empire. This is one foreign policy Trump is getting right.

Starmer, Macron and Merz are degrading their economies as they reduce critically needed social spending on the commons to fund a wildly unpopular war. No wonder far right, nationalistic political movements are nipping at their heels and may soon send them packing.

Europe has a pittance of America’s wealth to fund continuation of the war. Yet, the Starmer, Macron, Merz trio endlessly bleat that Ukraine can prevail, even get back its massive lost territory now forever part of Russia, if only they provide Ukraine more, more, more. They fear monger that Russia will come for them next unless they’re defeated in Ukraine. No responsible historian, political scientist or retired diplomat (without a job to protect) would support that delusional view.

Two things are certain. The economies and political stability of the UK, France, and Germany are being severely undermined by their leaders’ refusal to negotiate the war’s end, acknowledging Russia’s valid security concerns. Second, Ukraine descends deeper into failed state status, losing more cannon fodder and territory, every day the war grinds on.

What is not certain if Starmer, Macron and Merz do not come to their senses, is whether nuclear confrontation between Russia and NATO can be avoided. All 3 need to be forced to watch ‘Forrest Gump’ to learn that ‘Stupid is as stupid does.

Japan’s seismic history and the Westinghouse deal.

Letter to Ft.com : It almost feels impolite to point out some simple facts regarding your story “Westinghouse and US government strike $80bn nuclear reactor deal”. We are celebrating what Donald Trump hails as its “great friendship” between US and Japan, in addition to the election of our

first female prime minister, and an $80bn nuclear reactor deal — struck

by Washington and funded by Tokyo — all under the bright banner of what

appears to be a new era for our two countries.

Yet the simple fact remains,

whether we like it or not, that Japan is one of the most seismically active

countries in the world, which makes operating nuclear power plants far

riskier there than in the US.

The major nuclear players in both countries

— Westinghouse and Tokyo Electric Power (Tepco) — have faced bankruptcy or financial collapse. All publicly available, reliable data shows that solar power is significantly cheaper than new nuclear energy. Both our

countries’ leaders have issued similarly nationalistic statements on green

energy — President Trump even signed executive orders on “Unleashing

American Energy”, implicitly pointing to a common foe, namely China.

Warren Buffett once wrote that “more money has been stolen with the point

of a pen than at the point of a gun”. These nuclear power plant projects

will consume billions of dollars over the coming decades — long after

today’s leaders have left office. Future generations are being made the

“collateral” for decisions taken today.

FT 31st Oct 2025, https://www.ft.com/content/77769193-1cb0-4d8e-807a-e57936617de9

The Biggest Single Contributor to the UN Budget is also the Biggest Single Defaulter

By Thalif Deen, https://www.ipsnews.net/2025/10/the-biggest-single-contributor-to-the-un-budget-is-also-the-biggest-single-defaulter/?utm_source=email_marketing&utm_admin=146128&utm_medium=email&utm_campaign=The_Biggest_Single_Contributor_to_the_UN_Budget_is_also_the_Biggest_Single_Defaulter_As_Civil_Societ

UNITED NATIONS, Oct 31 2025 (IPS) – The United States, the largest single contributor to the UN budget, is using its financial clout to threaten the United Nations by cutting off funds and withdrawing from several UN agencies.

In an interview with Breitbart News U.S. Representative to the United Nations, Ambassador Mike Waltz said last week “a quarter of everything the UN does, the United States pays for”.

“Is there money being well spent? I’d say right now, no, because it’s being spent on all of these other woke projects, rather than what it was originally intended to do, what President Trump wants it to do, and what I want it to do, which is focus on peace.”

Historically, the United States has been the largest financial contributor, typically covering around 22% of the UN’s regular budget and up to 28% of the peacekeeping budget.

Still, ironically, the US is also the biggest defaulter. According to the UN’s Administrative and Budgetar Committee, member states currently owe $1.87 billion of the $3.5 billion in mandatory contributions for the current budget cycle.

And the US accounts for $1.5 billion of the outstanding balance.

Speaking to reporters in Kuala Lumpur last week, Secretary-General Antonio Guterres said: “We are not reforming the UN because of the liquidity crisis that is largely due to the reduction of payments from one main contributor, the United States”.

“What we are doing is recognizing that we can improve, that we can be more efficient, more cost-effective, more able to provide in full respect of our mandates to the people we care for in a more efficient way”.

“We are doing a number of reforms, making the Organization leaner but more effective. And that is the reason why there will be a number of reductions of positions in the Secretariat, but not the same everywhere.”

“And in particular, everything that relates to support to developing countries on the field in order for them to be able to overcome the present difficulties will not be reduced, on the contrary, will be increased,” he pointed out.

Mandeep S. Tiwana, Secretary General CIVICUS, a global civil society alliance, told IPS funding modalities for the UN need to be made simpler and also brought into the 21st century.

The present process, he pointed out, is too complicated and not easy to comprehend. Formulations for assessed and voluntary contributions are confusing and bureaucratic with some countries paying too much and others too little.

A simpler and fairer way would be assessed contributions be based on small percentage of a country’s Gross National Income. This would also allow formulations to be transparent and understandable by people around the world for whom the UN is exists,” declared Tiwana.

The five biggest funders of the UN, based on mandatory assessed contributions for the regular and peacekeeping budgets, are the United States, China, Japan, Germany, and the United Kingdom. These countries are responsible for a majority of the UN’s funding and are among the largest economies in the world.

United States: Pays the largest share, at around 22% for the regular budget and over 26% for peacekeeping.

China: The second-largest contributor, responsible for about 20% of the regular budget and nearly 19% of peacekeeping contributions.

Japan: Contributes approximately 7% to the regular budget and over 8% to peacekeeping.

Germany: Pays about 6% of the regular budget and 6% of the peacekeeping budget.

United Kingdom: Accounts for roughly 5% of both the regular and peacekeeping budgets.

Referring to the latest financial contribution, UN Deputy Spokesperson Farhan Haq told reporters October 30, “We thank our friends in Beijing for their full payment to the Regular Budget. China’s payment brings the number of fully paid-up Member States to 142,” (out of 193)

Asked how that money would help UN navigate through these difficult times, Haq said: “To be honest, any payments are helpful, but this is a very large payment– of more than $685 million– so it’s well appreciated.”

“And certainly, we thank the government in Beijing. But of course, we also stress that all governments need to pay their dues in full. You’ve seen the sort of financial pressures we’ve been under, and we do need full payments from all Member States,” he declared.

Kul Gautam, a former UN assistant secretary-general (ASG) and deputy director of UNICEF, pointed out that in 1985, Swedish Prime Minister Olof Palme proposed a simple remedy: no single country should pay—or be allowed to pay—more than 10% of the UN’s budget.

That, he said, would reduce dependence on any one donor while requiring modest increases from others. Ironically, Washington opposed it, fearing it might lose influence.

Asked for a clarification, he told IPS “it is my understanding that the assessed contributions to the UN regular budget are negotiated and approved by the UN General Assembly based on the recommendations of the GA’s Committee on Contributions, which determines a scale of assessments every three years based on a country’s “capacity to pay.”

The Committee on Contributions recommends assessment levels based on gross national income and other economic data, with a minimum assessment of 0.001% and a maximum assessment of 22%.

The scale of assessment of the UN regular budget does not need the approval of the Security Council, nor is it subject to veto by the P-5.

In the case of the UN’s peacekeeping budget, he said, the scale of assessment is based on a modification of the UN regular budget scale, with the P-5 countries assessed at a higher level than for the regular budget due to their role in authorizing and renewing peacekeeping missions.

Historically, the Security Council has authorized the UN General Assembly to create a separate assessed account for each peacekeeping operation. Thus, the Security Council definitely has a say in determining the peacekeeping budget.

In his interview with Breitbart News US Ambassador Mike Waltz also said: “And I would say to those who say, why don’t we just shut this thing down and walk away?”

“Well, I think we need it to be reformed in line with its potential that President Trump sees. And I think my answer would be: we need one place in the world where everybody can talk”.

President Trump is a president of peace, he said. He wants to keep us out of war. He wants to put diplomacy first. He wants to create deals.

“Well, there’s one place in the world, and that’s right here at the UN that the Chinese, the Russians, the Europeans, developing countries all over the world can come and do their best to hash things out,” declared.

In an October 17 statement, Guterres said: “My proposed programme budget for 2026 of 3.715 billion US dollars is slightly below the 2025 approved budget – excluding post re-costing and major construction projects in Nairobi and under the Strategic Heritage Plan.

This figure includes funding for 37 Special Political Missions – reflecting a net decrease due to the liquidation of the United Nations Assistance Mission for Iraq and the planned drawdown of the United Nations Transitional Assistance Mission in Somalia.

The proposed budget provides for 14,275 posts – and reflects our commitment to advance the three pillars of our work – peace and security, development, and human rights – in a balanced manner.

“We propose to continue supporting the Resident Coordinator System with a 53 million US dollars commitment authority for 2026 – identical to 2025.”

The 50 million US dollars grant for the Peacebuilding Fund is also maintained, he said..

IPS UN Bureau Report

Trump cuts Westinghouse reactors deal

one thing should be clear, significant financial risks are still there. Only four Westinghouse AP1000 units were ever financed in the US and remain a testament to nuclear power high risk, recurring and gross failure to financially control runaway cost-of-completion and time-to-completion estimates.

October 30, 2025, https://beyondnuclear.org/trump-cuts-westinghouse-reactors-deal/

On October 28, 2025, the Trump White House announced its commitment to stake at least $80 billion of US federal dollars to initiate yet another very risky run at new construction of Westinghouse Electric Company’s AP1000 nuclear stations. This is the follow-up to his May 23, 2025 executive orders to “unleash” more atomic power in the nation. Only this time, the Trump deal entitles the federal government, the designated buyer of the new reactors, to a 20% equity stake thereafter in Westinghouse’s returns in excess of $17.5 billion. Trump’s financing deal was cut with Westinghouse’s newest parent companies Brookfield Asset Management and Cameco, after the March 29, 2021 Westinghouse bankruptcy as of “the largest historic builder of nuclear power plants in the world.” At the time of the bankruptcy, Westinghouse was a wholly owned subsidiary of Japan’s Toshiba Corporation. Toshiba itself only narrowly escaped the financial meltdown.

On his latest visit to Asia, President Trump signed a nuclear deal with Japan newest, most hawkish and first woman Prime Minister, Saneae Takaichi, also announced on October 28th with an agreement to invest hundreds of billions of dollars in US critical infrastructure including in Trump’s pledge to domestically build new Westinghouse AP1000 reactor units and small modular reactors in the United States conditional on the involvement of Japanese contractors.

The Trump deal doesn’t specify just how much US taxpayer money will be spent on the new Westinghouse units Trump wants to build.

But one thing should be clear, significant financial risks are still there. Only four Westinghouse AP1000 units were ever financed in the US and remain a testament to nuclear power high risk, recurring and gross failure to financially control runaway cost-of-completion and time-to-completion estimates. Those new AP-1000 project orders were the only four units that managed to muster financing in South Carolina (V.C. Summer Units 2 & 3) and Georgia (Vogtle Units 3 & 4) of 34 US units announced in the 2007 launch with much ballyhoo of a so-called “nuclear renaissance.” The two projects’ financing was only made possible by the two state regulators indenturing their electricity ratepayers to Construction Work In Progress (CWIP) charges through their respective Public Utility Commissions levying a series of customer rate hikes in advance of electricity usage to guarantee construction financing. Otherwise, without public ratepayer on the hook for the advanced financing, a total of 30 other proposed new “advanced” reactor units (including 8 additional AP1000 units) were cancelled and withdrawn nationwide without a shovel in the ground.

South Carolina’s V.C. Summer AP1000 construction project was abandoned in 2017 with $10 billion in sunk costs and shrouded in FBI arrests, federal criminal convictions and guilty pleas by two high ranking SCANA utility executives, CEO Kevin Marsh, and Vice President Stephen Byrne, pleaded guilty to defraud South Carolina state regulators and its ratepayers after being charged with the crime by the U.S. Attorney’s office. Additionally, two Westinghouse Electric executives, Carl Churchman, a Vice President, pled guilty to making related false statements to the FBI investigators and sentenced to serve house detention and Jeffrey A. Benjamin, Senior Vice President for new plants and major products, who plead guilty to conspiracy to commit wire and securities fraud and serving one year and a day in federal prison.

Georgia’s Vogtle AP1000 two-unit project was eventually completed seven years behind the schedule to start operations in 2023 and 2024 with their original estimated combined cost of construction ballooning from $14 billion to an estimated $36.8 billion. Due to the expansion, massive rate hikes and prolonged delay, the Vogtle nuclear power station is now the largest and most expensive generator of electricity by atomic power in the United States.

In other related news, on Friday, October 24, 2025, South Carolina’s Santee Cooper Board of Directors unanimously voted to authorized the state-owned utility to sign a letter of intent to ask Brookfield Assets Management, previously mentioned as one of Westinghouse’s parent companies, to sign a Memorandum of Understanding (MOU) to take over the completion of the previously abandoned and only partially built nuclear reactors.

Santee Cooper’s CEO Jimmy Stanton was quoted by The State news service to pledge that, “There are no additional financial risks for our customers at all”. The Letter of Intent is meant to be the first step in a new permitting for the completion of construction project and then obtaining a federal license for full power operations. The original Nuclear Regulatory Commission (NRC) combined construction and operating license that Santee Cooper and SCE&G held is no longer valid following their 2017 abandonment of construction. The new licensee, assuming that to be Brookfield Assets or its qualified proxy, will need to go back to the US NRC and the state to reacquire the necessary permits to restart what is now called “the greatest construction failure in state history.” Santee Cooper has said it does not plan to hold the federal construction permit. Customers of Dominion Energy, the VC Summer Unit 1 new operator, are already on the hook to pay roughly 5% of their monthly bills for the original expansion project.

Furloughing Workers for Armageddon: Trump, Nuclear Weapons and the NNSA

To maintain and reproduce an arsenal of mass death and thanatotic desire, you need people of suspended moral principles. “Oversight matters,” Plonski remarks. “Reducing the federal workforce means increased risk in ensuring the reliability and safety of our nuclear stockpile.”

30 October 2025 Dr Binoy Kampmark, https://theaimn.net/furloughing-workers-for-armageddon-trump-nuclear-weapons-and-the-nnsa/

Instead of satirising nuclear war – a possible if difficult thing to do – the time has come to satirise the laying off and furlough of those who solemnly monitor and maintain such machinery fit, not for preserving life so much as ending it at a fiery, radiated terminus. If it’s not possible to totally disarm a nuclear inventory, it might be possible to reduce the forces behind them or render some idle. It turns out that this is happening in Freedom’s Land itself, the United States of America.

Those responsible for maintaining the US nuclear weapons arsenal have not been having the best of years. In February, President Donald Trump signed an executive order directing the heads of agencies to “promptly undertake preparations to initiate large-scale reductions in force, consistent with applicable law.” This was part of the now infamous Department of Government Efficiency Workforce Optimization Initiative. Within a few days, 300 employees at the National Nuclear Security Administration (NNSA), located within the Department of Energy, were fired. Prior to that, it had 2,000 staff and 55,000 contractors at its disposal.

The NNSA describes, as one of its “core missions” ensuring that the US “maintains a safe, secure, and reliable nuclear stockpile through the application of unparalleled science, technology, engineering, and manufacturing.” Easy to forget, on reading this, that we are not talking about agricultural supplies or lifesaving medicines, but over 3,000 nuclear warheads and ongoing production specific to that agency. “The Office of Defense programs,” the description goes on to say, “carries out NNSA’s mission to maintain and modernize the nuclear stockpile through the Stockpile Stewardship and Management System.”

NNSA deputy division director, Rob Plonski, was understandably upset that his citadel was being thinned. Ego, reputation and prowess in the nuclear field was at stake. “We cannot expect to project strength, deterrence and world dominance while simultaneously stripping away the federal workforce,” he moaned in a post on LinkedIn. He would have taken heart by the subsequent rescinding of the termination decision for all but 28 of the staff by NNSA acting director Teresa Robbins.

Trump, on the other hand, was having one of his more lucid moments, telling reporters on February 13 that nuclear forces should not be exempt from budgetary trimming. “There’s no reason for us to be building brand-new nuclear weapons. We already have so many, you could destroy the world 50 times over, 100 times over.” Daryl Kimball, executive director of the Arms Control Association, was having none of that. DOGE employees, he charged, were storming “in with absolutely no knowledge of what these departments are responsible for.” They barely realised that the purge was less to do with the Department of Energy than “the department of nuclear weapons.”

In October, the NNSA was again revisited by crisis, with the decision to furlough 1,400 employees due to that event distinct to US politics, the government shutdown. Till that point, the shutdown had lasted almost three weeks, with the Senate failing to pass a continuing resolution bill since October 1. Only 400 essential employees are being retained, labouring in patriotic sweat without pay. A spokesperson for the DOE explained that they would be working “to support the protection of property and safety of human life.”

Since its creation in 2000, the agency has had few such hiccups. “This has never happened before,” noted Energy Secretary Chris Wright during a news conference at the Nevada National Security Site on October 20. “This should not happen.” Wright, however, spoke of pursuing “creative ways” in paying the vast number of contractors, at least till the end of October.

Particular concern centres on the Pantex plant in Texas, the assembly and disassembling site for nuclear weapons, and the Y-12 National Security Complex in Tennessee, responsible for, according to the DOE, the retrieval and storage of nuclear materials, fuelling of naval reactors, and the performance of “complementary work for other government and private-sector entities.”

The NNSA had tried to argue that money be made available from previously passed spending bills to prevent the furlough. A DOE spokesperson proved icy in remarking that, “While the administration was able to identify funds to keep NNSA weapons laboratories, plants, and sites operating with our contractors, legal and budgetary limitations required the administration to begin furloughing NNSA federal employees.”

Therein lies the problem. To maintain and reproduce an arsenal of mass death and thanatotic desire, you need people of suspended moral principles. “Oversight matters,” Plonski remarks. “Reducing the federal workforce means increased risk in ensuring the reliability and safety of our nuclear stockpile.” With the support of 26 lawmakers, Rep. Dina Titus (D-Nev.) in her October 23 letter to Wright and NNSA administrator Brandon Williams similarly argued that the federal employees in question “play a critical oversight role in ensuring that the work required to maintain nuclear security is carried out in accordance with long-standing policy and the law.” Trump has also been fuzzy on the matter of nuclear weapons, acknowledging the nonsense of increasing the pile, yet simultaneously wanting tighter deadlines to deliver ever more modern weapons to the Pentagon.

This fantastically confused state of affairs throws up an interesting question: Why not turn the attention to reducing the stockpile itself and pause the euphemistically named modernisation process? A slimmer, sharper workforce for a more diminished, manageable arsenal of death that should never be used in any case. The National Security State remains, however, a tough, insatiable customer.

1 This Month

Website of the Week

New book – https://www.amazon.com/dp/1923372157?utm_source=substack&utm_medium=email

Now until to February 10, 2026 Radioactive waste storage in France: the debate is finally open! How to participate?

-

Archives

- January 2026 (74)

- December 2025 (358)

- November 2025 (359)

- October 2025 (377)

- September 2025 (258)

- August 2025 (319)

- July 2025 (230)

- June 2025 (348)

- May 2025 (261)

- April 2025 (305)

- March 2025 (319)

- February 2025 (234)

-

Categories

- 1

- 1 NUCLEAR ISSUES

- business and costs

- climate change

- culture and arts

- ENERGY

- environment

- health

- history

- indigenous issues

- Legal

- marketing of nuclear

- media

- opposition to nuclear

- PERSONAL STORIES

- politics

- politics international

- Religion and ethics

- safety

- secrets,lies and civil liberties

- spinbuster

- technology

- Uranium

- wastes

- weapons and war

- Women

- 2 WORLD

- ACTION

- AFRICA

- Atrocities

- AUSTRALIA

- Christina's notes

- Christina's themes

- culture and arts

- Events

- Fuk 2022

- Fuk 2023

- Fukushima 2017

- Fukushima 2018

- fukushima 2019

- Fukushima 2020

- Fukushima 2021

- general

- global warming

- Humour (God we need it)

- Nuclear

- RARE EARTHS

- Reference

- resources – print

- Resources -audiovicual

- Weekly Newsletter

- World

- World Nuclear

- YouTube

-

RSS

Entries RSS

Comments RSS