California achieves 100% renewable energy for 100 days.

On 100 out of 144 days since 8 March, California’s electricity has been supplied fully by

renewable energy for at least part of the day.

Power Technology 30th July 2024

https://www.power-technology.com/news/california-achieves-100-renewable-energy-for-100-days/

This nuclear waste site could soon host a massive solar installation

The Hanford Site in Washington state, a radioactive relic of the Manhattan Project and Cold War, was selected by DOE to be outfitted with up to 1GW of solar.

By Carrie Klein, 30 July 2024, https://www.canarymedia.com/articles/solar/this-nuclear-waste-site-could-soon-host-a-massive-solar-installation—

The U.S. Department of Energy announced plans last week to transform a contaminated former nuclear weapons production site into what could be the largest solar project in the country. The installation would stretch across up to 8,000 acres in south-central Washington state and boast up to 1 gigawatt of energy capacity — enough to power 750,000 homes.

One of the core challenges of building large solar installations is deciding where to put them. Local residents and farmers sometimes protest the use of agricultural land, while environmentalists urge caution in disturbing ecosystems. But this project location, known as the Hanford Site, is heavily contaminated from decades of atomic weapons production — first as part of the Manhattan Project and later during the Cold War.

Weapons production at Hanford created around 56 million gallons of radioactive and chemical waste, plus millions of cubic feet of solid waste and billions of gallons of less contaminated liquids. During production and upon Hanford’s decommissioning in the early 1990s, much of this waste was disposed of in concrete-lined pits, trenches, and ponds, and has since leached into the Columbia River basin, contaminating groundwater and causing health issues for locals.

Building solar at this location is “a great way to reuse land that has limited potential for other uses,” said Nels Johnson, senior advisor for renewable energy at The Nature Conservancy, who notes that “it means we’re not converting” prime farmland.

The project is part of the DOE’s new program Cleanup to Clean Energy, launched last year to help attain the climate goals in President Joe Biden’s 2021 executive order directing federal agencies to develop clean energy generation on their properties, with the goal of those agencies achieving 100 percent clean electricity by 2030.

The department announced the program’s first two projects — also solar installations — in June and July. One project will be located on 890 square miles of Idaho National Laboratory land and will feature 400 megawatts of solar capacity. The other will take up 2,400 acres of the Nevada National Security Site and has a capacity of 200 megawatts.

The Hanford project aims to generate the most energy by far — and, in addition to potentially becoming the largest solar project in the country, Johnson said that it would certainly be the largest on mine land, brownfield, or other degraded land.

Real estate negotiations are currently underway between the DOE and renewable energy developer Hecate Energy. Once an agreement is reached, Hecate will lead environmental reviews, including cultural resource surveys and consultations with local tribal nations, a DOE spokesperson told Canary Media. Hecate will also assess the impact of the proposed power generation on the grid to determine if any transmission upgrades are needed. These environmental and grid assessments could impact the ultimate size of the installation, according to the DOE.

The department declined to share a target timeline for the project.

In Benton County, where the Hanford Site sits, the Tri-City Development Council (TRIDEC) sees the solar installation as part of a larger transformation of the economy. The council, originally created to help diversify employment so the county was less dependent on federal funding, is planning several other renewable energy projects, along with “decarbonized manufacturing and industrial” projects, said Sean O’Brien, executive director at TRIDEC. “We very much envision that there will be a strong appetite for the electrons that this project will produce.”

Cleanup of the Hanford Site will be ongoing while the solar project moves forward into construction and operation in the coming years. “We can be doing both,” O’Brien said. The project itself will mostly be located on land that doesn’t require environmental remediation work, he said.

The Hanford Site is 560 square miles — about half the size of the state of Rhode Island. Since the late 1990s, workers have “cocooned,” or covered, seven nuclear reactors, removed 600 tons of contaminants from groundwater, and treated 32 billion gallons more. But decades of work still remain to fully remediate the site, O’Brien said. Adding solar to the site doesn’t change that, though it does at least put the land to productive use in the meantime.

China is installing the wind and solar equivalent of five large nuclear power stations per week

Instead of nuclear, solar is now intended to be the foundation of China’s new electricity generation system.

ABC Science / By technology reporter James Purtill, 16 July 24, https://www.abc.net.au/news/science/2024-07-16/chinas-renewable-energy-boom-breaks-records/104086640

In short:

China is installing record amounts of solar and wind, while scaling back once-ambitious plans for nuclear.

While Australia is falling behind its renewables installation targets, China may meet its end-of-2030 target by the end of this month, according to a report.

What’s next?

Energy experts are looking to China, the world’s largest emitter and once a climate villain, for lessons on how to rapidly decarbonise.

While Australia debates the merits of going nuclear and frustration grows over the slower-than-needed rollout of solar and wind power, China is going all in on renewables.

New figures show the pace of its clean energy transition is roughly the equivalent of installing five large-scale nuclear power plants worth of renewables every week.

A report by Sydney-based think tank Climate Energy Finance (CEF) said China was installing renewables so rapidly it would meet its end-of-2030 target by the end of this month — or 6.5 years early.

It’s installing at least 10 gigawatts of wind and solar generation capacity every fortnight.

By comparison, experts have said the Coalition’s plan to build seven nuclear power plants would add fewer than 10GW of generation capacity to the grid some time after 2035.

Energy experts are looking to China, the world’s largest emitter, once seen as a climate villain, for lessons on how to go green, fast.

“We’ve seen America under President Biden throw a trillion dollars on the table [for clean energy],” CEF director Tim Buckley said.

“China’s response to that has been to double down and go twice as fast.”

Smart Energy Council CEO John Grimes, who recently returned from a Shanghai energy conference, said China has decarbonised its grid almost as quickly as Australia, despite having a much harder task due to the scale of its energy demand.

“They have clear targets and every part of their government is harnessed to deliver the plan,” he said.

China accounts for about a third of the world’s greenhouse gas emissions. A recent drop in emissions (the first since relaxing COVID-19 restrictions), combined with the decarbonisation of the power grid, may mean the country’s emissions have peaked.

“With the power sector going green, emissions are set to plateau and then progressively fall towards 2030 and beyond,” CEF China energy policy analyst Xuyang Dong said.

So how is China building and connecting panels so fast, and what’s the role of nuclear in its transition?

Like building solar farms near Perth to power Sydney

Because its large cities of the eastern seaboard are dominated by apartment buildings, China hasn’t seen an uptake of rooftop solar like in Australia.

To find space for all the solar panels and wind turbines required for the nation’s energy needs, the planners of China’s energy transition have looked west, to areas like the Gobi Desert.

The world’s largest solar and wind farms are being built on the western edge of the country and connected to the east via the world’s longest high-voltage transmission lines.

These lines are so long they could span the length of our continent.

In Australian terms, it’s the equivalent of using solar panels near Perth to power homes in Sydney.

Mr Buckley said China’s approach was similar to the Australian one of developing regional “renewable energy zones” for large-scale electricity generation.

“They’re doing what Australia is doing with renewable energy zones but they’re doing it on steroids,” he said.

What about ‘firming’ the grid?

One of the issues with switching a grid to intermittent renewables is ensuring a steady supply of power.

In technical terms, this is the difference between generation capacity (measured in gigawatts) and actual energy output (measured in gigawatt-hours, or generation over time).

Renewables have a “capacity factor” (the ratio of actual output to maximum potential generation) of about 25 per cent, whereas nuclear’s is as high as 90 per cent.

So although China is installing solar and wind generation equivalent to five large nuclear power plants per week, their output is closer to one nuclear plant per week.

Renewables account for more than half of installed capacity in China, but only amount to about one-fifth of actual energy output over a year, the CEF’s Tim Buckley said.

To “firm” or stabilise the supply of power from its renewable energy zones, China is using a mix of pumped hydro and battery storage, similar to Australia.

“They’re installing 1GW per month of pumped hydro storage,” Mr Buckley said.

“We’re struggling to build the 2GW Snowy 2.0 in 10 years.”

There are some major differences between Australia and China’s approaches, though. Somewhat counterintuitively, China has built dozens of coal-fired power stations alongside its renewable energy zones, to maintain the pace of its clean energy transition.

China was responsible for 95 per cent of the world’s new coal power construction activity last year.

The new plants are partly needed to meet demand for electricity, which has gone up as more energy-hungry sectors of the economy, like transport, are electrified.

The coal-fired plants are also being used, like the batteries and pumped hydro, to provide a stable supply of power down the transmission lines from renewable energy zones, balancing out the intermittent solar and wind.

Despite these new coal plants, coal’s share of total electricity generation in the country is falling.

The China Energy Council estimated renewables generation would overtake coal by the end of this year.

The CEF’s Xuyang Dong said despite the country’s reliance on coal, “having China go green at this speed and scale provides the world with a textbook to do the same”.

“China is installing every week the equivalent of what we’re doing every year.”

Despite this speed, China wasn’t installing renewables fast enough to meet its 2060 carbon neutrality target, she added.

“According to our analysis, [the current rate of installation] is not ambitious enough for China.”

What about nuclear?

China is building new nuclear plants, although nowhere near as fast as it once intended.

In 2011, Chinese authorities announced fission reactors would become the foundation of the country’s electricity generation system in the next “10 to 20 years”.

But Japan’s 2011 Fukushima disaster prompted a moratorium on inland nuclear plants, which have to use river water for cooling and are more vulnerable to frequent flooding.

Meanwhile, over the following decade, solar became the cheapest electricity in the world.

From 2010 to 2020, the installed cost of utility-scale solar PV declined by 81 per cent on a global average basis.

As well as cheap, it was safe, which made solar farms quicker to build than nuclear reactors.

Instead of nuclear, solar is now intended to be the foundation of China’s new electricity generation system.

Authorities have steadily downgraded plans for nuclear to dominate China’s energy generation. At present, the goal is 18 per cent of generation by 2060.

China installed 1GW of nuclear last year, compared to 300GW of solar and wind, Mr Buckley said.

“That says they’re all in on renewables.

“They had grand plans for nuclear to be massive but they’re behind on nuclear by a decade and five years ahead of schedule on solar and wind.”

How is China transitioning so fast?

In June of this year, on the eve of the Coalition’s nuclear policy announcement, former Queensland Premier Annastacia Palaszczuk, who’s now a Smart Energy Council “international ambassador”, led a delegation of Australians to the world’s largest clean energy conference in Shanghai.

The annual Smart Energy Conference hosts more than 600,000 delegates across three days.

Its scale underlines China’s increasing dominance of the global clean energy economy and, for some attendees, prompted unenviable comparisons with Australia’s progress.

Mr Buckley, who was part of the delegation, said he was “blown away”.

“China is winning this race.”

John Grimes, the Smart Energy Council CEO who also attended, said Australia could learn from the Chinese government’s ability to execute a long-term, difficult and costly transition plan, rather than relying on market forces to find a solution.

“Australia’s transition is going too slow, there was a lost decade of action,” he said.

“The world today spends about $7 trillion a year on coal, gas and oil and that money is going to find a new home.

Who is going to be the economic winner in that global economic transition? It’s going to be China.”

He and other energy experts are frustrated with the progress of Australia’s transition, including the discussion of nuclear power and the “weaponisation of dissent” from community groups over new wind farms and transmission lines.

Stephanie Bashir, CEO of the Nexa energy advisory, said Australia’s transition was tangled in red tape.

“The key hold-up for a lot of projects is the slow planning approvals,” Ms Bashir, who also attended the conference, said.

“In China they decide they’re going to do something and then they go and do it.”

The Australian Energy Market Operator’s (AEMO) plan to decarbonise the grid and ensure the lights stay on when the coal-fired power stations close requires thousands of kilometres of new transmission lines and large-scale solar and wind farms.

Australia is installing about half the amount of renewables per year required under the plan.

Due to this shortfall, many experts say its unlikely to meet its 2030 target of 82 per cent renewables in the grid and 43 per cent emissions reduction.

“We need to build 6GW each year from now until each power station closes, and so far we’re only bringing online 3GW,” Ms Bashir said.

“If we identify some projects are nation-building … and we need them for transition, we just have to get on with it.”

Mr Buckley predicted China would accelerate its deployment of renewables.

“My forecast is it will lift 20 per cent per annum on current levels.”

Solar power will lead globally- says Rocky Mountain Institute (RMI)

‘Solar will very shortly overtake every other type of electricity generation and together with batteries, will electrify everything, everywhere’ says the Colorado-based Rocky Mountain Institute (RMI) in a new report on the cleantech revolution. Certainly renewables generation is now very cheap and solar PV deployment is doubling every 2-3 years, while battery storage, for backup, is doubling every year. Wind is also doing well around the world, with offshore wind leading in some locations, as I reported in an earlier post, and some new major projects going ahead.

Overall, RMI say that ‘clean technologies will continue to follow S-curves, cascading across sectors and geographies,’ with China, the world’s largest energy consumer, in the lead. It explains that ‘China, lacks oil and gas, and cleantech is a path to leadership, clean air, and zero emissions’. And so it will ‘continue to deploy cleantech rapidly’. So it sees China as ‘the pivot nation in the transition away from fossil fuels, and most areas of demand have clearly peaked there’. Also ‘peaks are showing up across the Global South, from S. America to South Africa & Thailand’.

It’s very optimistic stuff, reflecting the approach of RMI’s founder Dr Amory Lovins. Away with the old, in with the new- and fast. It says ‘S-curves imply that by 2030 solar and wind generation will triple to over 12,000 TWh and EVs will be two-thirds of car sales,’ pushing fossil use even further out. Taking a broad view , RMI claims that ‘New fossil electricity capacity peaked in 2010, oil and gas capex in 2014, and internal combustion engine car sales in 2017. Fossil demand peaked for industry in 2014, for buildings in 2018, most likely for electricity in 2023, and will shortly peak in transport’, and it says that this will continue, since ‘the drivers of growth are more powerful than the barriers. Falling cleantech costs, the energy security of eternal renewables, Chinese leadership, and a race to the top will continue to overwhelm a fragile fossil fuel system which wastes two-thirds of its primary energy and fails to pay for its externality costs’.

Well maybe, and China does have some very large solar PV projects, but it is not exactly a bastion of freedom! And in the short term at least there is still a lot of fossil fuel being used there, and elsewhere, as a new study from the UK Energy Institute (EI) and co-authors KPMG and Kearney notes. But it also notes that global renewable generation, excluding hydro, was up 13% to a record global high of 4,748TWh in 2023, due almost entirely by wind and solar expansion, led by China, which added 55% of all renewable generation additions in 2023.

Meantime, nuclear is still in the game, including in China. Indeed, the US Energy Information Administration says that ‘China continues rapid growth of nuclear power capacity’, although the chart it uses to support this assertion says it shows ‘annual installed’ net capacity, whereas, in fact it shows total capacity and growth in that has actually been slowing.

It’s 58GW now, only making a small overall power contribution in China- EIA says 5% in 2023. By contrast, as noted above, renewables are roaring ahead in China- growing 4 times faster than in the G7 countries overall, with wind and solar adding almost 300GW last year. And it is on track reach 1,200GW of wind and solar total capacity by end of 2024 – 6 years ahead of target.

Ever hopeful though, the nuclear lobby globally still looks to new technology, like Small Modular Reactors, to improve things, even if so far that doesn’t look too promising, with, as a Reuters article reports, there being project failures and high costs. But, SMR apologists say, it is early days yet- first designs often have problems and it takes time to get costs down. However, it would require some very radical cost reductions to compete with renewables, now at all time low costs, especially since they are likely to continue to getting cheaper. ………………………………………………………………………………..

Good thing we still have the free fusion reactor in the sky….with Ember reporting that global use of solar PV has expanded by 23% last year, and wind power by 10%, with renewables overall now supplying around 30% of global power and wind and solar projected to supply nearly 70% of global electricity by 2050. Moreover, some studies have suggested that renewables overall could supply around 100% of all power, or even all energy, by then, with solar playing a major role. https://renewextraweekly.blogspot.com/2024/07/solar-power-will-lead-globally-says-rmi.html

U.S. Solar and Wind Power Generation Tops Nuclear for First Time

By Charles Kennedy – Jul 11, 2024, https://oilprice.com/Latest-Energy-News/World-News/US-Solar-and-Wind-Power-Generation-Tops-Nuclear-for-First-Time.html?fbclid=IwZXh0bgNhZW0CMTEAAR36aY_qZHusiBuonQ8wnoYKA4biHRxGFjpdJPHNpgny-jFyIN5ZFM3NUL8_aem_2gvOQUW4tXrqTe8rUaH-xw

For the first time ever, U.S. electricity generation from utility-scale solar and wind exceeded nuclear power plants’ power output in the first half of 2024, according to data from energy think tank Ember quoted by Reuters columnist Gavin Maguire.

Electricity generation from solar and wind hit a record-high of 401.4 terawatt hours (TWh) between January and June 2024, surpassing the 390.5 TWh of power generated from nuclear power plants, Ember’s data showed.

Solar power generation jumped by 30% and electricity output from wind power rose by 10% in the first half of 2024, compared to the same period of last year.

In 2023, nuclear power accounted for 18.6% of U.S. electricity generation, while wind power output had a 10.2% share and solar accounted for 3.9% of total U.S. electricity output, according to data for 2023 from the U.S. Energy Information Administration (EIA).

Ember has estimated that the share of wind and solar grew to 16% in 2023, when nuclear was still the largest source of low-carbon electricity in the U.S.

However, expanding renewable energy capacity and record solar and wind power generation helped solar and wind combined to top nuclear as the biggest low-carbon electricity source during the first half of this year.

Early in 2024, the EIA said that wind and solar energy would lead growth in U.S. power generation for the next two years.

As a result of new solar projects coming on line this year, the administration forecast that U.S. solar power generation will surge by 75%, from 163 billion kilowatt-hours (kWh) in 2023 to 286 billion kWh in 2025. The EIA also expects that wind power generation will grow by 11% from 430 billion kWh in 2023 to 476 billion kWh in 2025.

In 2023, all renewable sources—wind, solar, hydro, biomass, and geothermal—accounted for 22% of total U.S. power generation.

“The Sun has won”: exponentially growing solar destroys nuclear, fossil fuels on price

Given Dutton’s claims about solar power costing more than nuclear are made ridiculous by the fact that solar’s break-even price has fallen by a factor of more than 1000 and the trend is continuing.

Meanwhile cost overruns in nuclear are endemic and SMR’s only exist in Dutton’s imagination.

By Noel Turnbull, Jul 11, 2024, https://johnmenadue.com/the-sun-has-won-exponentially-growing-solar-destroys-nuclear-fossil-fuels-on-price/—

It’s not known if Peter Dutton [ Australia’s pro-nuclear Opposition leader] reads The Economist but if he does, he must probably think from time to time that it is sometimes dangerously left wing.

In the 22 June issue, it had a special essay on solar power – headlined ‘The Sun Machine’. The sub-head was “An energy source which gets cheaper the more you use it marks a turning-point in industrial history’.

The essay is a total contradiction of almost everything Dutton is claiming about nuclear and renewable energy.

“What makes solar energy revolutionary is the rate of growth which brought it to this just-beyond the marginal state”, the essay says.

They cite a veteran energy analyst, Michael Liebreich, who shows that in 2004 it took a year to install a gigawatt of solar power capacity; in 2010 it took a month; in 2016 a week; and in single days in 2023 there were a gigawatt of installation worldwide.

Current projections are that solar will generate more electricity than all the world’s nuclear plants in 2026; than wind turbines in 2027; dams in 2028; gas-fired plants in 2026; and coal-fired ones in 2032.

All that well before Dutton’s nuclear plants – if at all – start generating power. Moreover, unlike nuclear power which notoriously always takes longer to build than predicted, predictions about the rate of solar power roll-out are consistently under-estimates.

The Economist points out that in in 2009 The International Energy Agency (IEA) predicted solar would increase from 23GW to 244GW by 2030. It hit that milestone in 2016 – less than a third of the predicted time. The world capacity was 1419GW by 2023.

Ironically, one of the few organisations which got their predictions roughly right was Greenpeace – yet even their prediction was an under-estimate.

Given Dutton’s claims about solar power costing more than nuclear are made ridiculous by the fact that solar’s break-even price has fallen by a factor of more than 1000 and the trend is continuing. Meanwhile cost overruns in nuclear are endemic and SMR’s only exist in Dutton’s imagination.

Dutton is stronger on ideology and outrageous claims than economics, but the manufacture of photovoltaics is a classic example of the benefits of mass production – benefits which have always eluded the nuclear power industry.

As The Economist points out solar cells are standardised products all made in basically the same way and “they have no moving parts at all, let alone the fiendish complexity of a modern turbine.”

“Manufacturers compete on cost, by either making cells that make fractionally more electricity, by either making cells that make fractionally out of a given amount of sunshine or which cost less.”

Economics 101 teaches us that a commoditised product does not lead to more and more aggressive competition on the supply side – simply in this case by getting more electricity out of any given amount of sunshine or by costing less.

Rob Carlson, a technology investor, told The Economist: “There is no other energy-generation tech where you can install one million or one of the same thing depending on your application.”

“The Sun has won” he says.

The Economist said: “From the mid-1970 to the early 2020s cumulative shipments of photovoltaics increased by a factor of a million which is 20 doublings. At the same time prices dropped by a factor of 500. That is a 27% decrease in cost of doubling of installed capacity, which means a halving of costs every time installed capacity increases by 360%.

Adair Turner, an eminent economist and financial services executive, was Chair of Britian’s Climate Change Committee which was set up to help transition to zero emissions.

He told The Economist: “We totally failed to see that solar would come down so much.”

BloombergNEF estimated, in 2015, that the cost for solar on a global basis was $122 per MWH – higher than on shore wind and coal. Today both solar and onshore wind are almost half the cost of coal.

Meanwhile, Dutton has welcomed Keir Starmer’s election win by pointing to his support for nuclear power. Which, given that the UK has already installed nuclear power, the cautious Starmer is unlikely to announce that he is closing it down.

Moreover, Starmer’s major problem with nuclear is managing the spiralling delays in, and cost of, nuclear plants being constructed following typical Tory blunders.

The question which Dutton needs to answer is why he knows more about nuclear and solar power than The Economist reporters, Bloomberg, Adair Turner, Rob Carlson, many major investment funds and the overwhelming majority of Australian scientists?

He might ponder all that while the Murdoch media is becoming a tad critical of him – criticising his policy on supermarket divestment and speculating on who might be the Liberal Party leader if Dutton loses the next election.

Meanwhile, notwithstanding their doubts about Dutton’s chances and policies (other than nuclear) The Australian never totally loses its manic opposition to anything progressive. The inimitable Greg Sheridan opined on The Australian front page (6/7) that Labour had not won but the Tories had lost. Partly true obviously, but his piece was enough to prompt the subs to headline the piece with “Self-described socialist is set to drag Britain far to the left”.

Sheridan also rehearsed his regular hates and speculated how it would all come undone.

Jeremy Corbyn would love that to be the case but Starmer not so.

Perhaps the funniest lines in Sheridan’s’ piece were: “Starmer is brainy and works hard. Too deep immersion in the law has rendered it impossible for Starmer to write felicitous prose or create memorable images.”

From a journalist who year after year simply reproduces the same old opinions on the same old subjects that is, to say the least, a bit much.

The nuclear and renewable myths that mainstream media can’t be bothered challenging

Mark Diesendorf, Jul 4, 2024, https://reneweconomy.com.au/the-nuclear-and-renewable-myths-that-mainstream-media-cant-be-bothered-challenging/

Nuclear energy proponents are attempting to discredit renewable energy and promote nuclear energy and fossil gas in its place. This article refutes several myths they are disseminating that are receiving little or no challenge in the mainstream media.

Myth: Renewables cannot supply 100% electricity

Denmark, South Australia and Scotland already obtain 88, 74 and 62 per cent of their respective annual electricity generations from renewables, mostly wind. Scotland actually supplies 113 per cent of its electricity consumption from renewables; the difference between its generation and consumption is exported by transmission line.

All three jurisdictions have achieved this with relatively small amounts of hydroelectricity, zero in South Australia. Given the political will, all three could reach 100% net renewables generation by 2030, as indeed two northern states of Germany have already done. The ‘net’ means that they trade some electricity with neighbours but on average will be at 100% renewables.

Computer simulations by several research groups – using real hourly wind, solar and demand data spanning several years – show that the Australian electricity system could be run entirely on renewable energy, with the main contributions coming from solar and wind. System reliability for 100% renewables will be maintained by a combination of storage, building excess generating capacity for wind and solar (which is cheap), key transmission links, and demand management encouraged by transparent pricing.

Storage to fill infrequent troughs in generation from the variable renewable sources will comprise existing hydro, pumped hydro (mostly small-scale and off-river), and batteries. Geographic dispersion of renewables will also assist managing the variability of wind and solar. For the possibility of rare, extended periods of Dunkelflaute (literally ‘dark doldrums’), gas turbines with stores of biofuels or green hydrogen could be kept in reserve as insurance.

Myth: Gas can fill the gap until nuclear is constructed

As a fuel for electricity generation, fossil gas in eastern Australia is many times more expensive per kilowatt-hour than coal. It is only used for fuelling gas turbines for meeting the peaks in demand and helping to fill troughs. For this purpose, it contributes about 5% of Australia’s annual electricity generation. But, as storage expands, fossil gas will become redundant in the electricity system.

The fact that baseload gas-fired electricity continues temporarily in Western Australia and South Australia is the result of peculiar histories that will not be repeated. Unlike the eastern states, WA has a Domestic Gas Reservation Policy that insulates customers from the high export prices of gas.

However, most new gas supplies would have to come from high-cost unconventional sources. South Australia’s ancient, struggling, baseload, gas-fired power station, Torrens Island, produces expensive electricity. It will be closed in 2026 and replaced with renewables and batteries.

Myth: Nuclear energy can co-exist with large contributions from renewables

This myth has two refutations:

- Nuclear is too inflexible in operation to be a good partner for variable wind and solar. Its very high capital cost necessitates running it constantly, not just during periods of low sun or wind. Its output can only be ramped up and down slowly, and it’s expensive to do that.

- On current growth trends of renewables, there will be no room for nuclear energy in South Australia, Victoria or NSW. The 2022 shares of renewables in total electricity generation in each of these states were 74%, 37% and 33% respectively.

Rapid growth from these levels is likely. It’s already too late for nuclear in SA. Provided the growth of renewables is not deliberately suppressed in NSW and Victoria, these states too could reach 100% renewables before the first nuclear power station comes online.

As transportation and combustion heating will be electrified, demand for electricity could double by 2050. This might offer generating space for nuclear in the 2040s in Queensland (23% renewables in 2022) and Western Australia (20% renewables in 2022). However, the cost barrier would remain.

Myth: There is insufficient land for wind and solar

The claim by nuclear proponents that wind and solar have “vast land footprints” is misleading. Although a wind farm can span a large area, its turbines, access road and substation occupy a tiny fraction of that area, typically about 2%.

Most wind farms are built on land that was previously cleared for agriculture and are compatible with all forms of agriculture. Off-shore wind occupies no land.

Solar farms are increasingly being built sufficiently high off the ground to allow sheep to graze beneath them, providing welcome shade. This practice, known as agrivoltaics, provides additional farm revenue, which is especially valuable during droughts. Rooftop solar occupies no land.

Myth: The longer lifetime of nuclear reactors hasn’t been taken into account

The levelised cost of energy method – used by CSIRO, AEMO, Lazard and others – is the standard way of comparing electricity generation technologies that perform similar functions.

It permits the comparison of coal, nuclear and firmed renewables. It takes account automatically of the different lifetimes of different technologies.

Myth: We need baseload power stations

The recent claim that nuclear energy is not very expensive “when we consider value” is just a variant of the old, discredited claim that we need baseload power stations, i.e. those that operate 24/7 at maximum power output for most of the time.

The renewable system, including storage, delivers the same reliability, and hence the same value, as the traditional system based on a mix of baseload and peak-load power stations.

When a nuclear power reactor breaks down, it can be useless for weeks or months. For a conventional large reactor rated at 1000 to 1600 megawatts, the impact of breakdown on electricity supply can be disastrous.

Big nuclear needs big back-up, which is expensive. Small modular reactors do not exist––not one is commercially available or likely to be in the foreseeable future.

Concluding remarks

We do not need expensive, dangerous nuclear power, or expensive, polluting fossil gas. A nuclear scenario would inevitably involve the irrational suppression of renewables.

The ban on nuclear power should be maintained because nuclear never competes in a so-called ‘free market’. Renewables – solar, wind and existing hydro – together with energy efficiency, can supply all Australia’s electricity.

Mark Diesendorf is Honorary Associate Professor at the Environment & Society Group in the School of Humanities & Languages and Faculty of Arts, Design & Architecture at UNSW. First published in Pearls and Irritations. Republished with permission of the author.

When it comes to power, solar is about to leave nuclear and everything else in the shade

In Australia, solar is pushing down prices

Australia’s energy market operator says record generation from grid-scale renewables and rooftop solar is pushing down wholesale electricity prices.

Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University July 2, 2024 https://theconversation.com/when-it-comes-to-power-solar-is-about-to-leave-nuclear-and-everything-else-in-the-shade-233644

Opposition leader Peter Dutton might have been hoping for an endorsement from economists for his plan to take Australian nuclear.

He shouldn’t expect one from The Economist.

The Economist is a British weekly news magazine that has reported on economic thinking and served as a place for economists to exchange views since 1843.

By chance, just three days after Dutton announced plans for seven nuclear reactors he said would usher in a new era of economic prosperity for Australia, The Economist produced a special issue, titled Dawn of the Solar Age.

Whereas nuclear power is barely growing, and is shrinking as a proportion of global power output, The Economist reported solar power is growing so quickly it is set to become the biggest source of electricity on the planet by the mid-2030s.

By the 2040s – within this next generation – it could be the world’s largest source of energy of any kind, overtaking fossil fuels like coal and oil.

Solar’s off-the-charts global growth

Installed solar capacity is doubling every three years, meaning it has grown tenfold in the past ten years. The Economist says the next tenfold increase will be the equivalent of multiplying the world’s entire fleet of nuclear reactors by eight, in less time than it usually takes to build one of them.

To give an idea of the standing start the industry has grown from, The Economist reports that in 2004 it took the world an entire year to install one gigawatt of solar capacity (about enough to power a small city). This year, that’s expected to happen every day.

Energy experts didn’t see it coming. The Economist includes a chart showing that every single forecast the International Energy Agency has made for the growth of the growth of solar since 2009 has been wrong. What the agency said would take 20 years happened in only six.

The forecasts closest to the mark were made by Greenpeace – “environmentalists poo-pooed for zealotry and economic illiteracy” – but even those forecasts turned out to be woefully short of what actually happened.

And the cost of solar cells has been plunging in the way that costs usually do when emerging technologies become mainstream.

The Economist describes the process this way:

As the cumulative production of a manufactured good increases, costs go down. As costs go down, demand goes up. As demand goes up, production increases – and costs go down further.

Normally, this can’t continue. In earlier energy transitions – from wood to coal, coal to oil, and oil to gas – it became increasingly expensive to find fuel.

But the main ingredient in solar cells (apart from energy) is sand, for the silicon and the glass. This is not only the case in China, which makes the bulk of the world’s solar cells, but also in India, which is short of power, blessed by sun and sand, and which is manufacturing and installing solar cells at a prodigious rate.

Solar easy, batteries more difficult

Batteries are more difficult. They are needed to make solar useful after dark and they require so-called critical minerals such as lithium, nickel and cobalt (which Australia has in abundance).

But the efficiency of batteries is soaring and the price is plummeting, meaning that on one estimate the cost of a kilowatt-hour of battery storage has fallen by 99% over the past 30 years.

In the United States, plans are being drawn up to use batteries to transport solar energy as well as store it. Why build high-voltage transmission cables when you can use train carriages full of batteries to move power from the remote sunny places that collect it to the cities that need it?

Solar’s step change

The International Energy Agency is suddenly optimistic. Its latest assessment released in January says last year saw a “step change” in renewable power, driven by China’s adoption of solar. In 2023, China installed as much solar capacity as the entire world did in 2022.

The world is on track to install more renewable capacity over the next five years than has ever been installed over the past 100 years, something the agency says still won’t be enough to get to net-zero emissions by 2050.

That would need renewables capacity to triple over the next five years, instead of more than doubling.

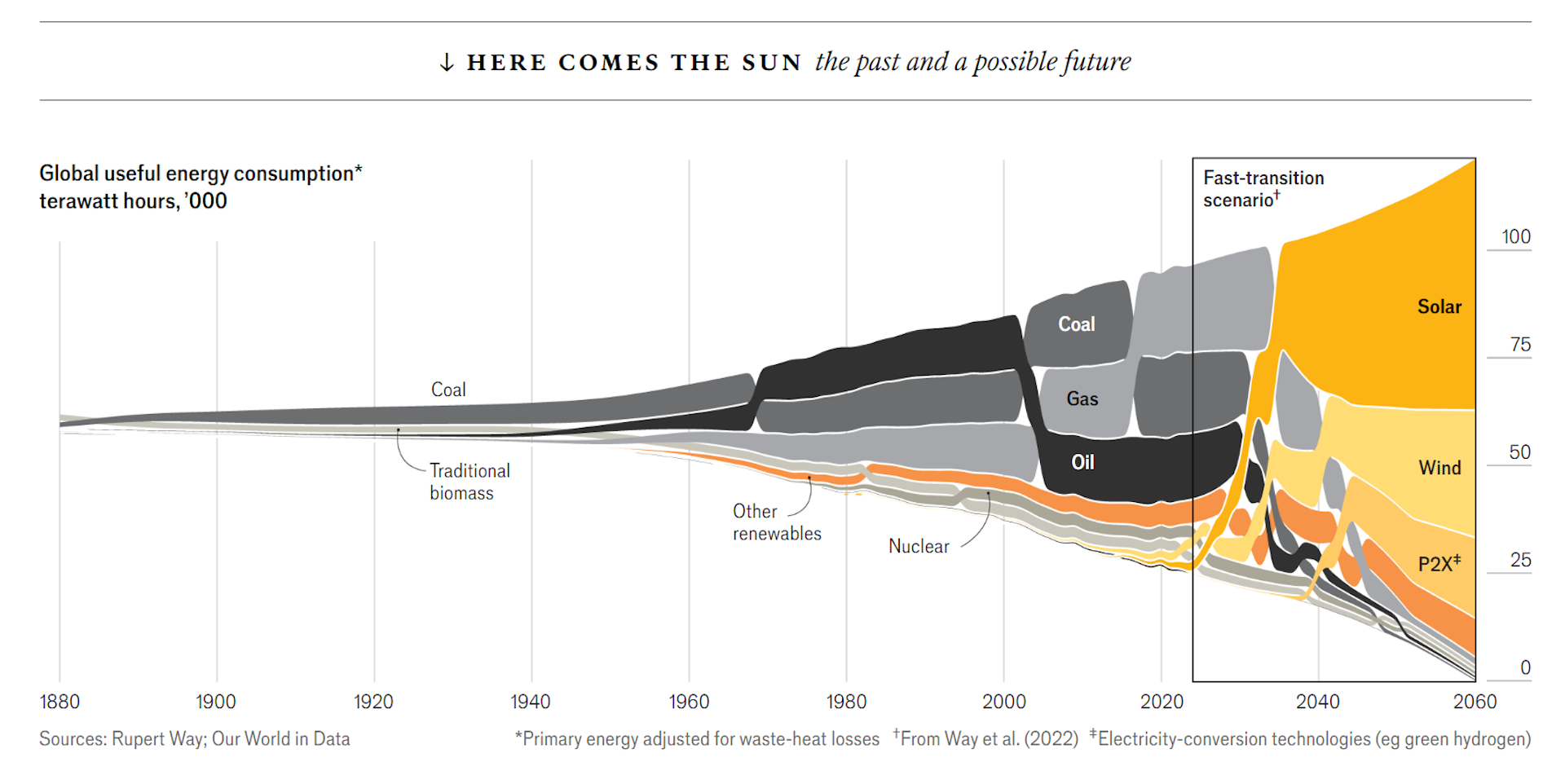

Oxford University energy specialist Rupert Way has modelled a “fast transition” scenario, in which the costs of solar and other new technologies keep falling as they have been rather than as the International Energy Agency expects.

He finds that by 2060, solar will be by far the world’s biggest source of energy, exceeding wind and green hydrogen and leaving nuclear with an infinitesimally tiny role.

In Australia, solar is pushing down prices

Australia’s energy market operator says record generation from grid-scale renewables and rooftop solar is pushing down wholesale electricity prices.

South Australia and Tasmania are the states that rely on renewables the most. They are the two states with the lowest wholesale electricity prices outside Victoria, whose prices are very low because of its reliance on brown coal.

It is price – rather than the environment – that most interests The Economist. It says when the price of something gets low people use much, much more of it.

As energy gets really copious and all but free, it will be used for things we can’t even imagine today. The Economist said to bet against that is to bet against capitalism.

“They just fit in with what we do:” Australian farmers reap rewards as they play host to wind and solar

ReNewEconomy Liv Casben, Jun 29, 2024

Renewables in agriculture are gaining momentum across the nation as Australia pushes to reach its net-zero emissions target by 2050.

Australia’s energy market operator has declared renewables as the most cost-effective way of reaching net-zero targets in the grid, but just how much of the load will be carried by the farming sector remains unclear.

Across pockets of the nation, farmers are already doing their bit to reduce their carbon footprint.

“Anecdotally, we have seen a huge increase in farmers seeking renewables projects as farmers seek to increase the productivity of their farms,” Farmers for Climate Action’s Natalie Collard told AAP.

“Renewables offer drought-proof income, and drought-proof income keeps farms going through the toughest of times.”

The Lee family has farmed at Glenrowan West for 150 years, but for the past three years they’ve also added solar to the mix.

A German-based company leases the land from the Lees and maintains the solar panels, which run alongside the sheep farming operation.

“The lessee basically runs it just as another paddock, the sheep go in just as they would under any other farming operation,” Gayle Lee said. “We haven’t found there to be any noticeable loss of production.”

……………………………………………………. Karin Stark, who will host the annual Renewables in Agriculture conference in Toowoomba next week, says consultation is key to farmers playing a “critical role” in the renewables transition and keeping everyone happy…………… more https://reneweconomy.com.au/they-just-fit-in-with-what-we-do-farmers-reap-rewards-as-they-play-host-to-wind-and-solar/?fbclid=IwZXh0bgNhZW0CMTEAAR0qML5s3XgsQ3EZd5pJl15CdGXQ60-BC3TLkIVpcaWkgLsBSarHkHoPUYI_aem_OC5kzgz0cTiwWtnLVva56A

Why we are heading for a globally connected electricity system based on renewable energy

renewable globalism is coming, so home-sited renewables are needed to protect British energy security

DAVID TOKE, JUN 21, 2024, https://davidtoke.substack.com/p/why-we-are-heading-for-a-globally

Slowly but surely the world is creeping towards global interconnection. That could make a global 100 per cent renewable energy system work a lot better. There would be reductions in the amount of storage needed and consequent reductions in cost. That is what academics are saying, including work done by electrical engineers based at the University of Birmingham (UK). Put simply, different parts of the world could power each other at different times of the day and night.

Solar power will become the dominant energy source. As Professor Christian Breyer says: ‘yes, solar & battery will be the central backbone of global energy supply, even more so in the sunbelt where two-third of world population live’. ‘Globalism’ will rule the electricity delivery system. Globalism already exists in the form of the international oil, and increasingly, natural gas industry. However, now with the development of HVDC transmission systems which minimise grid-based power losses, electricity can be transported efficiently over very great distances.

But the incremental march of international electricity interconnections is gradually pushing us in the direction of a global electricity system. It is happening incrementally. A new globalism based on renewable energy has great advantages, according to academics who have modelled the concept.

Of course, we should strive for energy security in the UK. This means wind power especially in the UK, supplemented by as much solar power as we can generate. Other renewable energy resources are potentially substantial in the UK. This includes geothermal energy, tidal stream energy and wave power, all of which are in greater or lesser stages of development. Of course the more renewables are deployed in the UK, the more we shall be able to profit from international trading in renewable energy.

As I say in my recently published book ‘Energy Revolutions’ (pages 36-37):

‘One interesting approach is to imagine providing 100 per cent of energy from renewables in the context of a globally interconnected electricity system. This would have the advantage of connecting areas where it is daytime with areas where it is night, as well as more and less windy zones. In recent decades, new engineering solutions for interconnection involving high-voltage direct current have emerged. These allow the possibility of (economically) transmitting electricity across thousands of miles while minimising electricity losses. A group of researchers has modelled the possibilities for a global system to provide 100%RE. They concluded that, compared to systems that are not globally interconnected, a globally interconnected system would reduce storage costs for 100%RE by 50 per cent and reduce the costs by 20 per cent.’

Incremental progress towards global interconnection is happening. I’m not necessarily talking about much-publicised plans to connect up the UK directly with solar pv from North Africa – that may or may not happen in some form or other sometime in the future – and perhaps never at all in a direct sense. Really, discussion of plans like that trivialises discussion about increasing international links in electricity supply.

What I am rather talking about, for the moment are the plans, which have begun to be implemented, to connect up North Africa and with southern Europe. Developments like that could lead to greater linkage of British electricity systems. On the one hand, British international electricity interconnection with the continent of Europe is expanding and on the other hand, African interconnection with European states is also occurring. But this will be indirect, rather than direct, connections between the UK and Africa.

The latest incremental change in the progress towards completion of the interconnector between Crete and Attica. Meanwhile, the European Commission is offering financial backing to interconnector projects between Italy and Tunisia, one between Egypt and Greece, and another between Greece, Cyprus and Israel. This programme runs parallel with the European Commission target that member states should have interconnections worth at least 15 per cent of their national electricity consumption by 2015.

The UK, if anything, is expanding rather faster than this, with the bulk of our current (9.8 GW) of international interconnector capacity having been commissioned since 2010. According to OFGEM new international interconnectors are set to increase this capacity by over 50 per cent by 2030. These are all projects with our neighbours: Norway, Ireland, Denmark, France, Germany and Belgium.

Of course we are still some way off having a globally interconnected system. However the spread of renewable energy which is building up to an astonishingly rapid rate is turbocharging the growth of interconnectors. This is because the variable nature of renewable energy encourages greater interconnection.

Globalism is slowly happening in electricity interconnection, perhaps not through dramatic direct projects, but gradually. Britain has a stake in this in that it can export renewable energy production, thus reducing excess renewable energy production. We should continue our practice of issuing fixed price contracts for renewable energy to enure that UK consumers get a good deal. But a global system of interconnection will reduce the need to store so much energy because it can import excess renewable energy from other places – perhaps places which are thousands of miles away.

Surging Renewables Push French Energy Prices Negative, Shutting Down Nuclear Plants

by Rahul Kumar, June 15, 2024, in Business and Finance, https://theubj.com/business/surging-renewables-push-french-energy-prices-negative-shutting-down-nuclear-plants/

French energy prices recently plunged into negative territory, reaching a four-year low of -€5.76 per megawatt-hour in an Epex Spot auction, Bloomberg reported. This unusual occurrence was driven by an excess of renewable energy production combined with reduced demand, particularly over the weekend. The surplus in renewable power led to some French nuclear plants going offline.

Renewable Energy Surge and Market Impact

The drop in day-ahead energy prices underscores the profound impact that renewable energy, particularly wind and solar power, is having on the European energy market. As renewable energy production surged, especially during periods of low demand, it created an oversupply that forced prices down. This imbalance pressured Electricité de France (EDF), the state-owned utility company, to temporarily shut down several nuclear reactors to avoid generating excess power that could not be sold profitably. Initially, three nuclear plants were halted, with plans to take three more offline.

A Pan-European Issue

This phenomenon is not isolated to France. Other European countries, including Spain and those in the Scandinavian region, also experience similar shutdowns of nuclear reactors due to excess renewable energy generation. The continent’s push to decarbonize energy grids has accelerated the deployment of renewable infrastructure. However, the lack of adequate battery technology and investment to store surplus energy has created pricing inefficiencies, leading to occurrences of negative prices.

Germany’s Experience

Germany, a leader in renewable energy adoption, has also faced negative energy prices. SEB Research reported in May that solar power generation in Germany had outpaced demand, leading to similar pricing challenges. Despite these issues, Germany has been more aggressive in its rollout of renewable energy compared to France. This aggressive approach has helped Germany mitigate some of the market inefficiencies seen in France.

France’s Renewable Energy Rollout

In contrast, France’s rollout of renewable energy has been slower. Paris has installed around 45 gigawatts of wind and solar capacity, which is behind the targets set by the European Commission. The slower adoption rate has contributed to the country’s struggle to balance its energy supply and demand efficiently.

Political and Economic Implications

The political landscape in France could further impact the renewable energy sector. The far-right National Rally party, which is poised to make significant gains in upcoming domestic elections, has pledged to slash renewable subsidies and halt the expansion of the wind power industry. Such political developments could slow down the already modest pace of France’s renewable energy rollout, potentially leading to more significant market inefficiencies and continued reliance on traditional energy sources.

Broader Challenges

The situation in France highlights the broader challenges associated with transitioning to renewable energy. While the shift towards cleaner energy is essential for reducing carbon emissions and combating climate change, it also necessitates advancements in energy storage solutions and a more balanced energy mix to ensure market stability and efficiency. Without these advancements, countries may continue to experience negative pricing and the associated operational challenges.

Conclusion

The recent plunge into negative energy prices in France due to an oversupply of renewable energy underscores the complex dynamics of the modern energy market. As Europe continues to push towards decarbonization, the need for robust energy storage solutions and strategic market management becomes increasingly critical. The experiences of France and other European countries serve as a reminder of the growing pains associated with the global shift towards sustainable energy.

Farmers who graze sheep under solar panels say it improves productivity. So why don’t we do it more?

Guardian, by Aston Brown, 14 June 24

Allowing livestock to graze under renewable developments gives farmers a separate income stream, but solar developers have been slow to catch on.As a flock of about 2,000 sheep graze between rows of solar panels, grazier Tony Inder wonders what all the fuss is about. “I’m not going to suggest it’s everyone’s cup of tea,” he says. “But as far as sheep grazing goes, solar is really good.”

Inder is talking about concerns over the encroachment of prime agricultural land by ever-expanding solar and windfarms, a well-trodden talking point for the loudest opponents to Australia’s energy transition.

But on Inder’s New South Wales property, a solar farm has increased wool production. It is a symbiotic relationship that the director of the National Renewables in Agriculture Conference, Karin Stark, wants to see replicated across as many solar farms as possible as Australia’s energy grid transitions away from fossil fuels.

“It’s all about farm diversification,” Stark says. “At the moment a lot of us farmers are reliant on when it’s going to rain, having solar and wind provides this secondary income.”

In exchange, the panels provide shelter for the sheep, encourage healthier pasture growth under the shade of the panels and create “drip lines” from condensation rolling off the face of the panels.

“We had strips of green grass right through the drought,” Dubbo sheep grazier Tom Warren says. Warren has seen a 15% rise in wool production due to a solar farm installed on his property more than seven years ago.

Despite these success stories, a 2023 Agrivoltaic Resource Centre report authored by Stark found that solar grazing is under utilised in Australia because developers, despite saying they intend to host livestock, make few planning adjustments to ensure that happens……………………………………………………………………………….

According to an analysis by the Clean Energy Council, less than 0.027% of land used for agriculture production would be needed to power the east coast states with solar projects – far less than the one-third of all prime agricultural land that the rightwing thinktank the Institute of Public Affairs has claimed will be “taken over” by renewables. That argument, which has been heavily refuted by experts, has been taken up by the National party, whose leader, David Littleproud, said regional Australia had reached saturation point with renewable energy developments.

Queensland grazier and the chair of the Future Farmers Network, Caitlin McConnel, has sold electricity to the grid from a dozen custom-built solar arrays on her farm’s cattle pastures for more than a decade.

“Trial and error” and years of modifications have made them structurally sound around cattle and financially viable in the long-term, she says.

“As far as I know, we are the only farm to do solar with cattle,” McConnel says. “It’s good land, so why would we just lock it up just for solar panels?” https://www.theguardian.com/australia-news/article/2024/jun/13/farmers-who-graze-sheep-under-solar-panels-say-it-improves-productivity-so-why-dont-we-do-it-more

A global review of Battery Storage: the fastest growing clean energy technology today

Energy Post 27th May 2024 by IEA

The IEA report “Batteries and Secure Energy Transitions” looks at the impressive global progress, future projections, and risks for batteries across all applications. 2023 saw deployment in the power sector more than double. Strong growth occurred for utility-scale batteries, behind-the-meter, mini-grids, solar home systems, and EVs. Lithium-ion batteries dominate overwhelmingly due to continued cost reductions and performance improvements. And policy support has succeeded in boosting deployment in many markets (including Africa).

Further innovations in battery chemistries and manufacturing are projected to reduce global average lithium-ion battery costs by a further 40% by 2030 and bring sodium-ion batteries to the market. The IEA emphasises the vital role batteries play in supporting other clean technologies, notably in balancing intermittent wind and solar.

New successes include the fact that solar PV plus batteries is now competitive with new coal-fired power in India and, in the next couple years, should become competitive with new coal in China and new natural gas-fired power in the U.S. Looking ahead, deployment must increase sevenfold by 2030. The prospects are good: if all announced plants are built on time this would be sufficient to meet the battery requirements of the IEA’s net-zero scenario in 2030. And although, today, the supply chain for batteries is very concentrated, the fast-growing market should create new opportunities for diversifying those supply chains.

Batteries are an essential part of the global energy system today and the fastest growing energy technology on the market

Battery storage in the power sector was the fastest growing energy technology in 2023 that was commercially available, with deployment more than doubling year-on-year.

Strong growth occurred for utility-scale battery projects, behind-the-meter batteries, mini-grids and solar home systems for electricity access, adding a total of 42 GW of battery storage capacity globally. Electric vehicle (EV) battery deployment increased by 40% in 2023, with 14 million new electric cars, accounting for the vast majority of batteries used in the energy sector.

Despite the continuing use of lithium-ion batteries in billions of personal devices in the world, the energy sector now accounts for over 90% of annual lithium-ion battery demand. This is up from 50% for the energy sector in 2016, when the total lithium-ion battery market was 10-times smaller. With falling costs and improving performance, lithium-ion batteries have become a cornerstone of modern economies, underpinning the proliferation of personal electronic devices, including smart phones, as well the growth in the energy sector. In 2023, there were nearly 45 million EVs on the road – including cars, buses and trucks – and over 85 GW of battery storage in use in the power sector globally.

Lithium-ion batteries dominate battery use due to recent cost reductions and performance improvements…………………………………………………………….

‘Offshore wind farms could have averted Fukushima disaster’

A global review led by the University of Surrey reveals that offshore wind farms could have prevented the Fukushima disaster and are now a cheaper energy alternative than nuclear power

Dimitris Mavrokefalidis, 05/30/2024 , https://www.energylivenews.com/2024/05/30/offshore-wind-farms-could-have-averted-fukushima-disaster/

A review conducted by researchers at the University of Surrey has concluded that offshore wind farms could have averted the Fukushima nuclear disaster by maintaining the cooling systems and preventing a meltdown.

The study highlights that wind farms are less vulnerable to earthquakes than nuclear power plants.

Suby Bhattacharya, Professor of Geomechanics at the University of Surrey, emphasised that wind power provides abundant clean energy and can enhance the safety and reliability of other facilities.

The review indicates that wind energy is now more cost-effective due to reduced construction costs and improved methods to minimise environmental impact.

The report finds that new wind farms can produce energy at a significantly lower cost than new nuclear power stations.

In the UK, the lifetime cost of generating wind power has dropped from £160/MWh to £44/MWh, covering all expenses from planning to decommissioning.

Professor Bhattacharya said: “What makes wind so attractive is that the fuel is free, and the cost of building turbines is falling. There is enough of it blowing around the world to power the planet 18 times over.

“Our report shows the industry is ironing out practical challenges and making this green power sustainable, too.”

2

TODAY. Jobs jobs jobs in the nuclear industry – but is it true?

Go to Google news for nuclear information, and you’ll be swamped with glowing stories from the World Nuclear Association, the IAEA, and the big corporate media outlets – all about the wonderful future for the nuclear industry- –

all those jobs! including in the lovely nuclear weapons industry.

Jobs in renewable energy. This year’s report finds that renewable energy employment worldwide has continued to expand – to an estimated 13.7 million direct and indirect jobs in 2022. We can expect the creation of many millions of additional jobs in the coming years and decades. https://mc-cd8320d4-36a1-40ac-83cc-3389-cdn-endpoint.azureedge.net/-/media/Files/IRENA/Agency/Publication/2023/Sep/IRENA_Renewable_energy_and_jobs_2023.pdf?rev=4f65518fb5f64c9fb78f6f60fe821bf2

Jobs in nuclear power. I have not been able to find any kind of authoritative report on global jobs in nuclear power. I did find one source (on Quora) stating that each nuclear reactor in construction provides 1400-1800 jobs, and in operation 400 -700 jobs. The nuclear industry claims many more, but for construction, we must remember – this is all in the rather distant future.

The figure below is a prediction from many years ago. If we are to believe the nuclear lobby, this prediction should change rapidly.

What we do know is that at present, renewable energy jobs are increasing exponentially, and nuclear power building is almost at a standstill.

The figure on the left is also from many years ago. But I doubt that much has changed.

Of course – this is all about the actual reactors. There are many jobs in uranium mining, milling, transport etc, and of course, in nuclear weapons-making

The quality of jobs.

In energy efficiency there are many interesting and clean jobs. Also, workers know that they are contributing to a healthier planet – something to be proud of.

In renewable energy the jobs are relatively clean and healthy, and there’s again, the knowledge of being in an alternative to the polluting industries – coal and nuclear.

In nuclear energy and nuclear fuel, the workers are involved in the risky area of ionising radiation. There’s a huge amount of documentation on this. It is NOT a healthy job, though I suppose that it’s better to be a highly paid nuclear executive or lobbyist, safe in a nice office.

I doubt that nuclear workers can get much satisfaction about “helping the planet”, as the “peaceful” nuclear industry is so dirty, dangerous, and intimately connected with nuclear weapons.

No doubt some nuclear workers get paid a lot more than renewable energy workers do. But, there’s real value in knowing that your contribution to society is a clean and positive one.

1 This Month

of the week – Shut Down Drone Warfare!

Tell the Ukrainian Government to Drop Prosecution of Peace Activist Yurii Sheliazhenko

Petition to revoke the licensing of the Near Surface Nuclear Disposal Facility (NSDF) at Chalk River. https://www.ourcommons.ca/petitions/en/Petition/Details?Petition=e-7247

To see nuclear-related stories in greater depth and intensity – go to https://nuclearinformation.wordpress.com

-

Archives

- April 2026 (7)

- March 2026 (251)

- February 2026 (268)

- January 2026 (308)

- December 2025 (358)

- November 2025 (359)

- October 2025 (376)

- September 2025 (257)

- August 2025 (319)

- July 2025 (230)

- June 2025 (348)

- May 2025 (261)

-

Categories

- 1

- 1 NUCLEAR ISSUES

- business and costs

- climate change

- culture and arts

- ENERGY

- environment

- health

- history

- indigenous issues

- Legal

- marketing of nuclear

- media

- opposition to nuclear

- PERSONAL STORIES

- politics

- politics international

- Religion and ethics

- safety

- secrets,lies and civil liberties

- spinbuster

- technology

- Uranium

- wastes

- weapons and war

- Women

- 2 WORLD

- ACTION

- AFRICA

- Atrocities

- AUSTRALIA

- Christina's notes

- Christina's themes

- culture and arts

- Events

- Fuk 2022

- Fuk 2023

- Fukushima 2017

- Fukushima 2018

- fukushima 2019

- Fukushima 2020

- Fukushima 2021

- general

- global warming

- Humour (God we need it)

- Nuclear

- RARE EARTHS

- Reference

- resources – print

- Resources -audiovicual

- Weekly Newsletter

- World

- World Nuclear

- YouTube

-

RSS

Entries RSS

Comments RSS

{kind=link}